{kind=link}

The U.S. labor market demonstrated remarkable endurance in April, with job gains outpacing expectations and private sector expansion reaching its strongest point in over a year. This resilience has resonated through financial markets, propelling the S&P 500 to its sixth consecutive weekly gain and a fresh record high. As the Federal Reserve maintains a steady interest rate policy, the focus now turns to upcoming inflation and retail data to gauge the sustainability of this momentum.

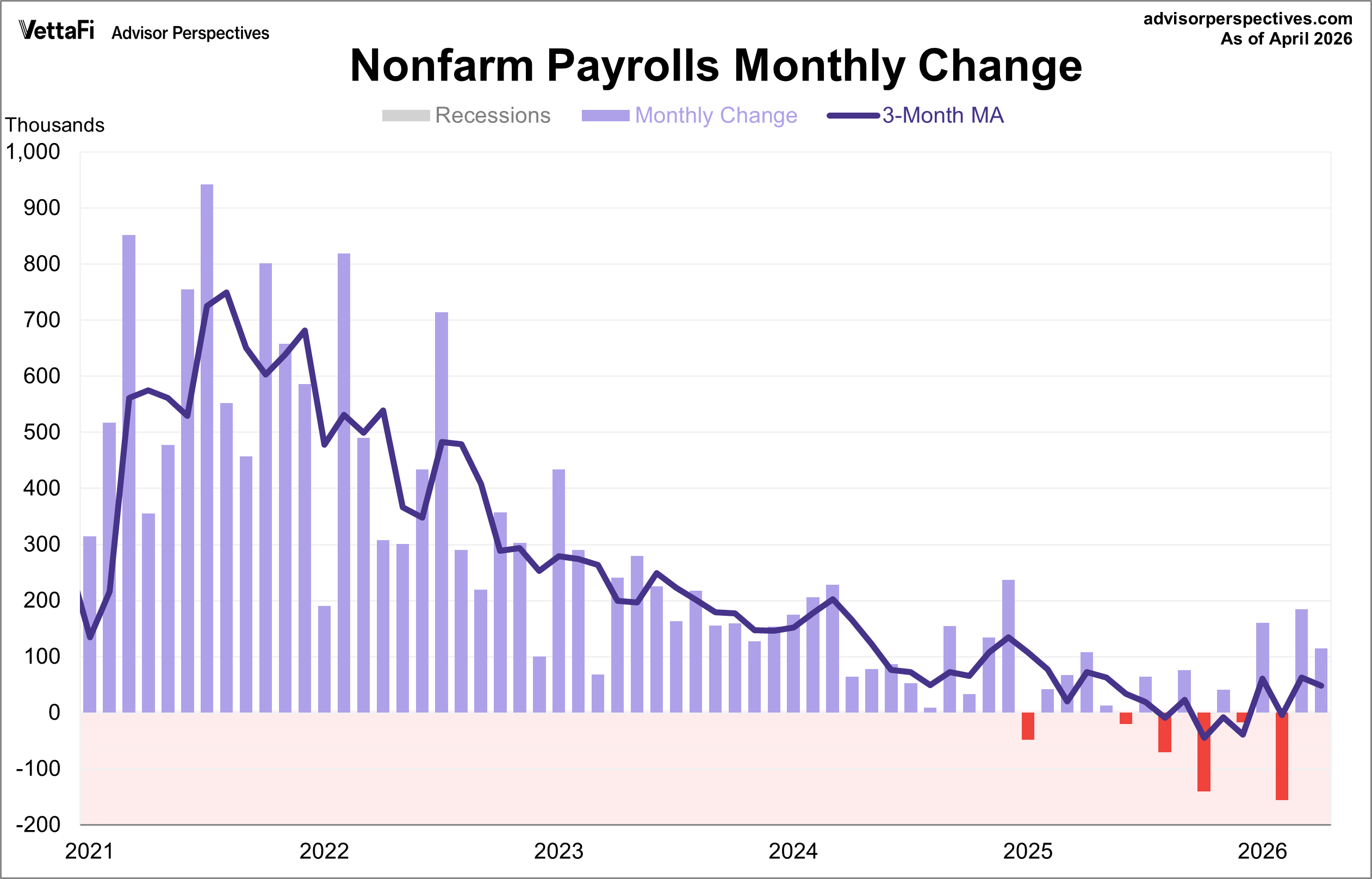

Labor Market Resilience: April Employment Data

The U.S. labor market maintained its resilience in April, with job gains nearly doubling expectations. The Bureau of Labor Statistics reported the economy added 115,000 jobs last month, significantly outpacing the projected 46,000. Additionally, March figures were revised upward to 185,000, while February saw a downward revision to a loss of 156,000. The unemployment rate held steady at 4.3%, as expected.

This latest data suggests the labor market has entered 2026 on a solid foundation, averaging 76,000 new jobs per month While the timeline for potential rate cuts remains extended, these results provide the Federal Reserve with the flexibility to shift their focus to the inflation side of their dual mandate.

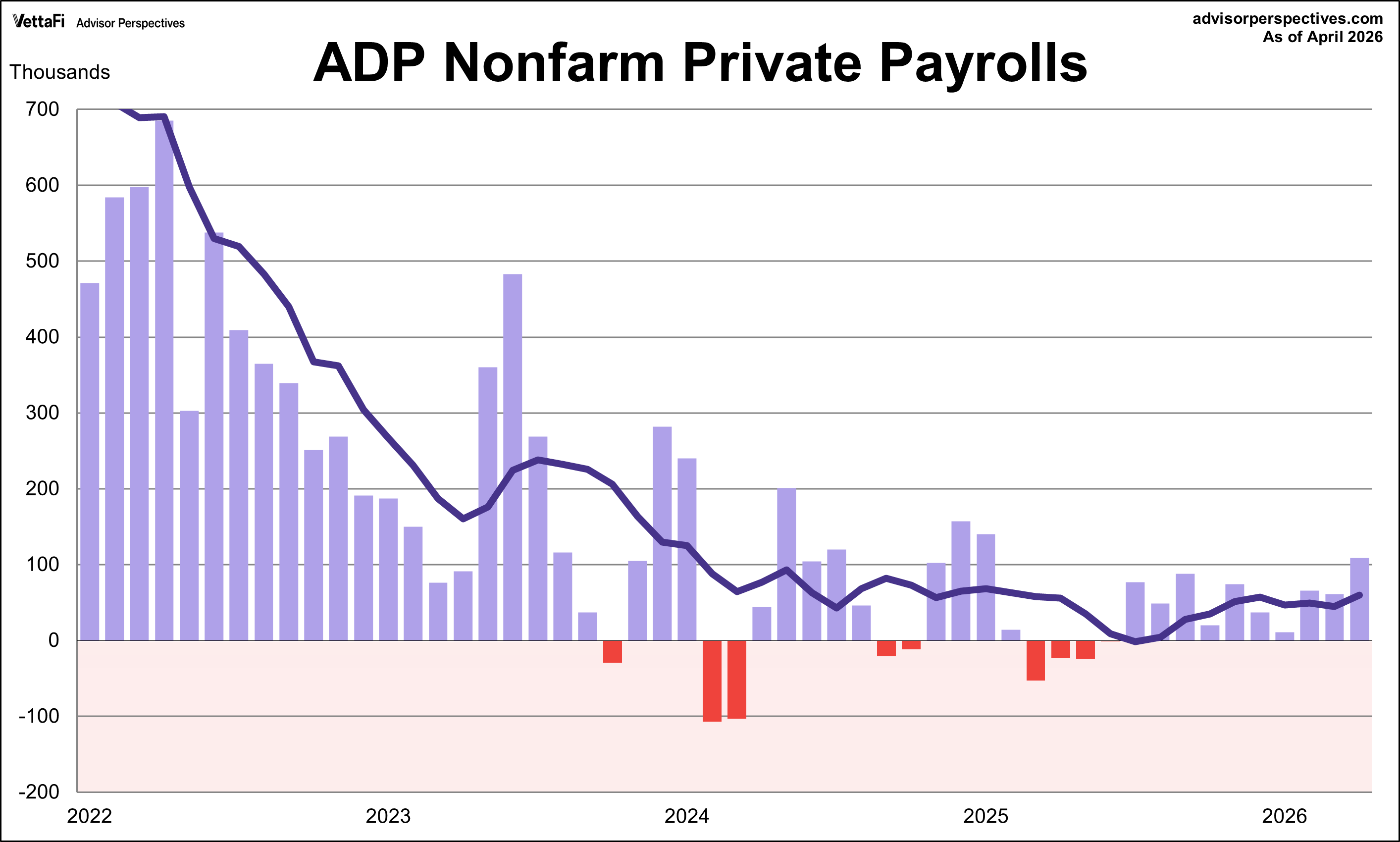

Private Sector Momentum: ADP Employment Report

The April ADP National Employment Report offered further evidence of a healthy U.S. labor market, as private sector payrolls rose by 109,000. While slightly below the anticipated 118,000, this figure represents the strongest monthly gain since January 2025 and marks the tenth consecutive month of expansion for the private sector.

The job gains were most notable among small (1-19 employees) and large (500+ employees) employers, which added a combined 85,000 positions. However, mid-size companies exhibited relative weakness as they appeared to lack both the robust resources of their larger counterparts and the operational agility of smaller firms.

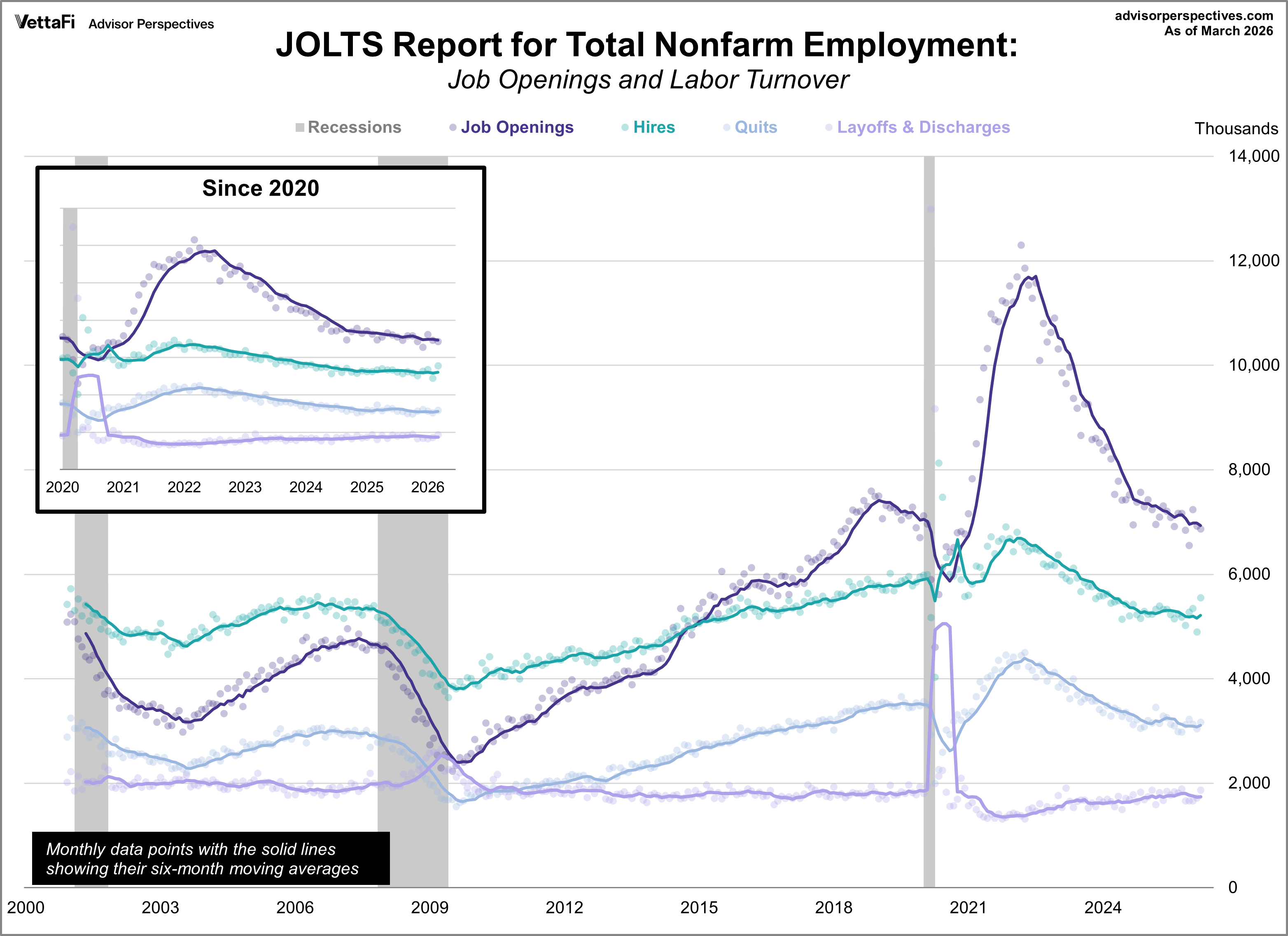

Hiring Trends and Vacancies: March JOLTS Summary

March’s JOLTS report reinforced the narrative of a solid labor market, revealing that the hiring rate reached a nearly two-year peak even as job openings saw a minor dip. Although vacancies fell to 6.866 million, marking the fourth decrease within a five-month span, the figure remained slightly above the 6.860 million forecast.

The report also highlighted that the ratio of job openings to unemployed workers climbed to 0.95, indicating that there are now more job seekers than available positions. Nevertheless, a surge in hiring to its highest level since February 2024 more than offset the previous month’s decline.

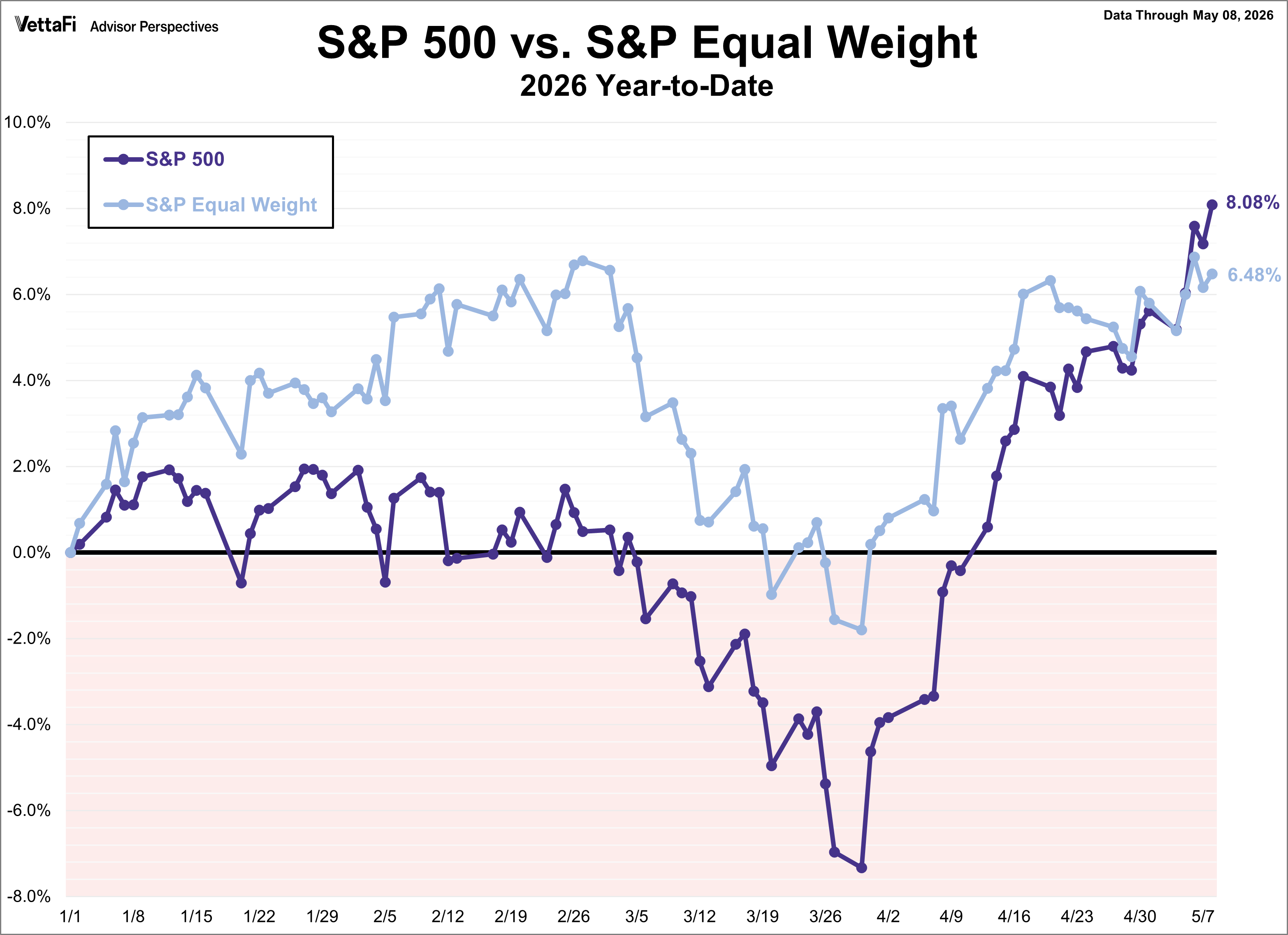

Market Reactions

The S&P 500 capped last week off with another record high, flirting with the 7,400 milestone. With a 2.3% weekly gain, the index has now climbed for six consecutive weeks, matching its longest winning streak since October 2024. As a result, the SPDR S&P 500 ETF Trust (SPY) rose 2.3% last week. Meanwhile, the S&P Equal Weight Index was up 0.6% from the previous week and the Invesco S&P 500® Equal Weight ETF (RSP) rose 0.6%.

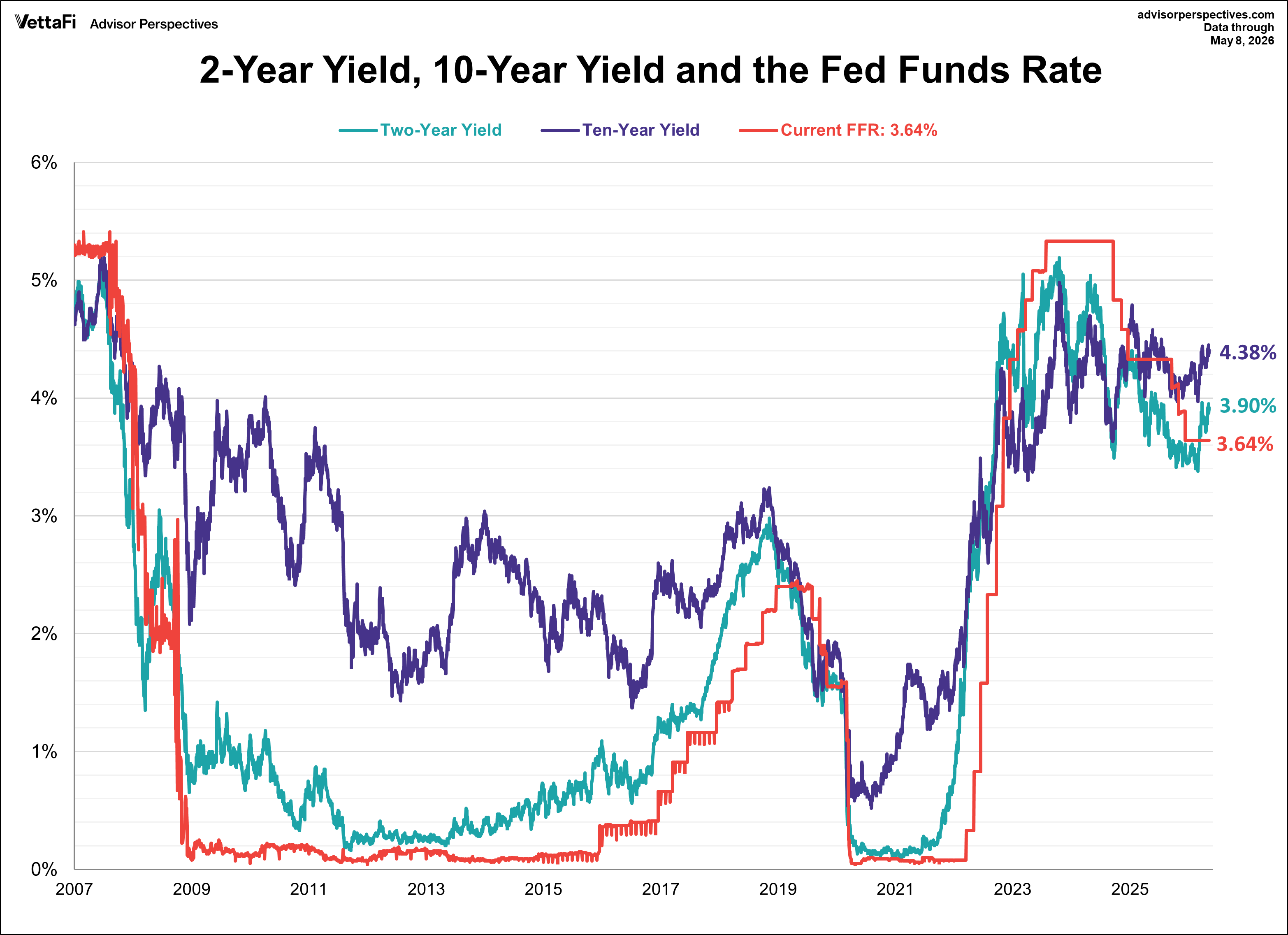

The 10-year Treasury yield finished the week at 4.38%, while the 2-year note finished at 3.90%.

Expectations for next month’s Federal Reserve meeting suggest the central bank will keep interest rates steady. According to the CME FedWatch Tool, there is a 94% probability that rates will be maintained, compared to just a 6% chance of a 25 basis point reduction. Current market projections indicate that further adjustments, including potential cuts or hikes, are unlikely through the end of 2026 and into 2027.

Looking Ahead: Economic Data for the Week of May 11, 2026

- Monday: Existing Home Sales (Apr)

- Tuesday: Consumer Price Index (Apr), NFIB Small Business Optimism Index (Apr), Short Term Energy Outlook (May)

- Wednesday: Producer Price Index (Apr)

- Thursday: Weekly Jobless Claims, Retail Sales (Apr)

- Friday: NY Empire State Manufacturing Index (May), Industrial Production (Apr)

Originally published on Advisor Perspectives

For more news, information, and strategy, visit ETF Trends.