{kind=link}

The U.S. economy continues to display a complex mix of resilience and persistence. While third-quarter growth surged at its fastest pace in two years, the Federal Reserve’s preferred inflation metrics remain stubbornly above target, complicating the path for future rate cuts. Meanwhile, consumers are showing signs of cautious optimism, with sentiment reaching a five-month high despite lingering concerns over price pressures. As markets brace for next week’s FOMC meeting, this snapshot breaks down the latest shifts in GDP, inflation, and consumer behavior.

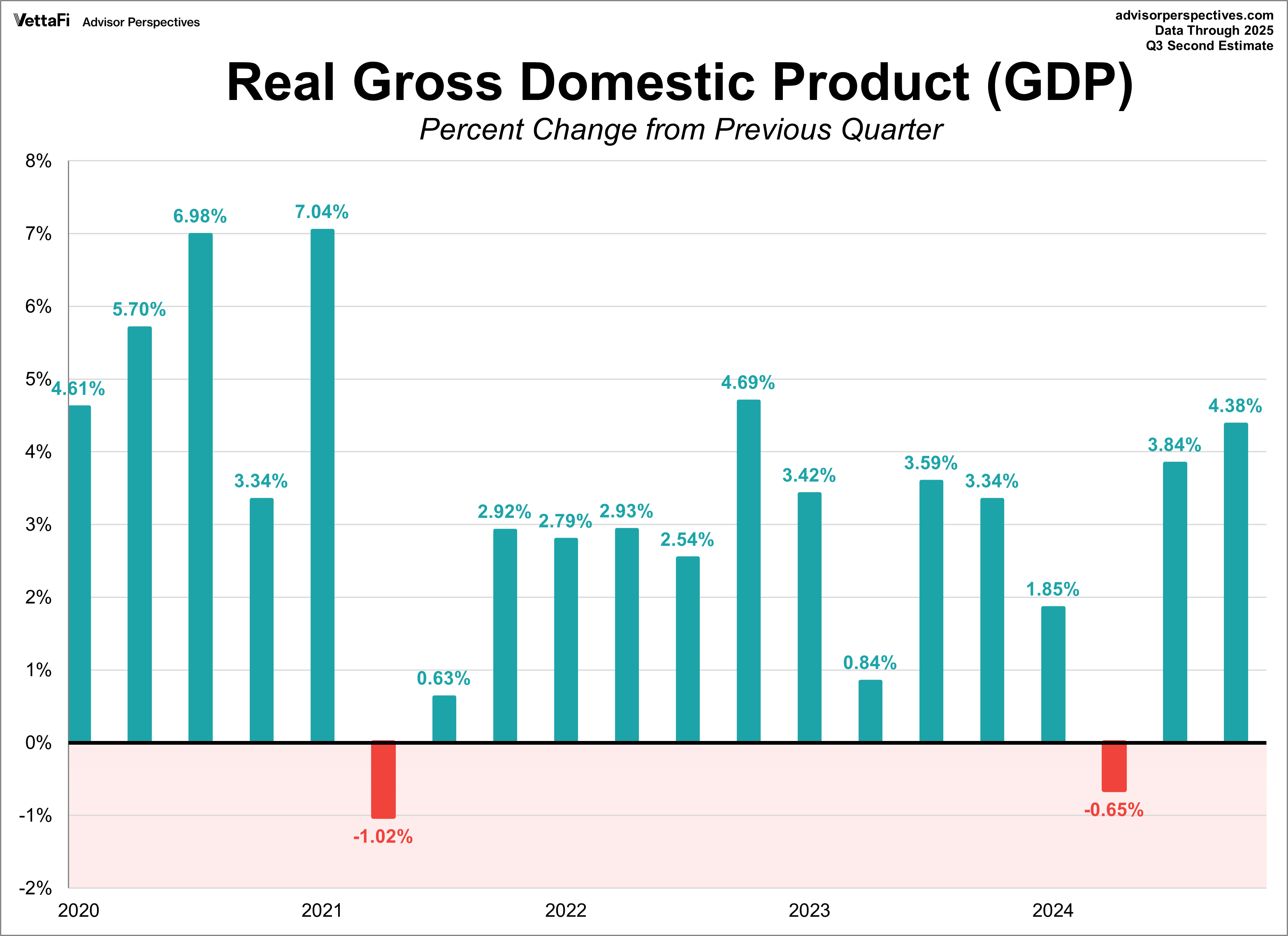

Gross Domestic Product (GDP)

The U.S. economy showed robust growth in the third quarter, posting its strongest reading in two years. The BEA’s updated estimate of real GDP, the inflation-adjusted measure of all goods and services produced, increased at an annual rate of 4.4% from July to September. This marks an uptick from the second quarter’s 3.8% growth and exceeded the 4.3% forecast from last month’s estimate. The expansion was driven by broad-based increases in consumer spending, exports, government spending, and investment, alongside a decline in imports.

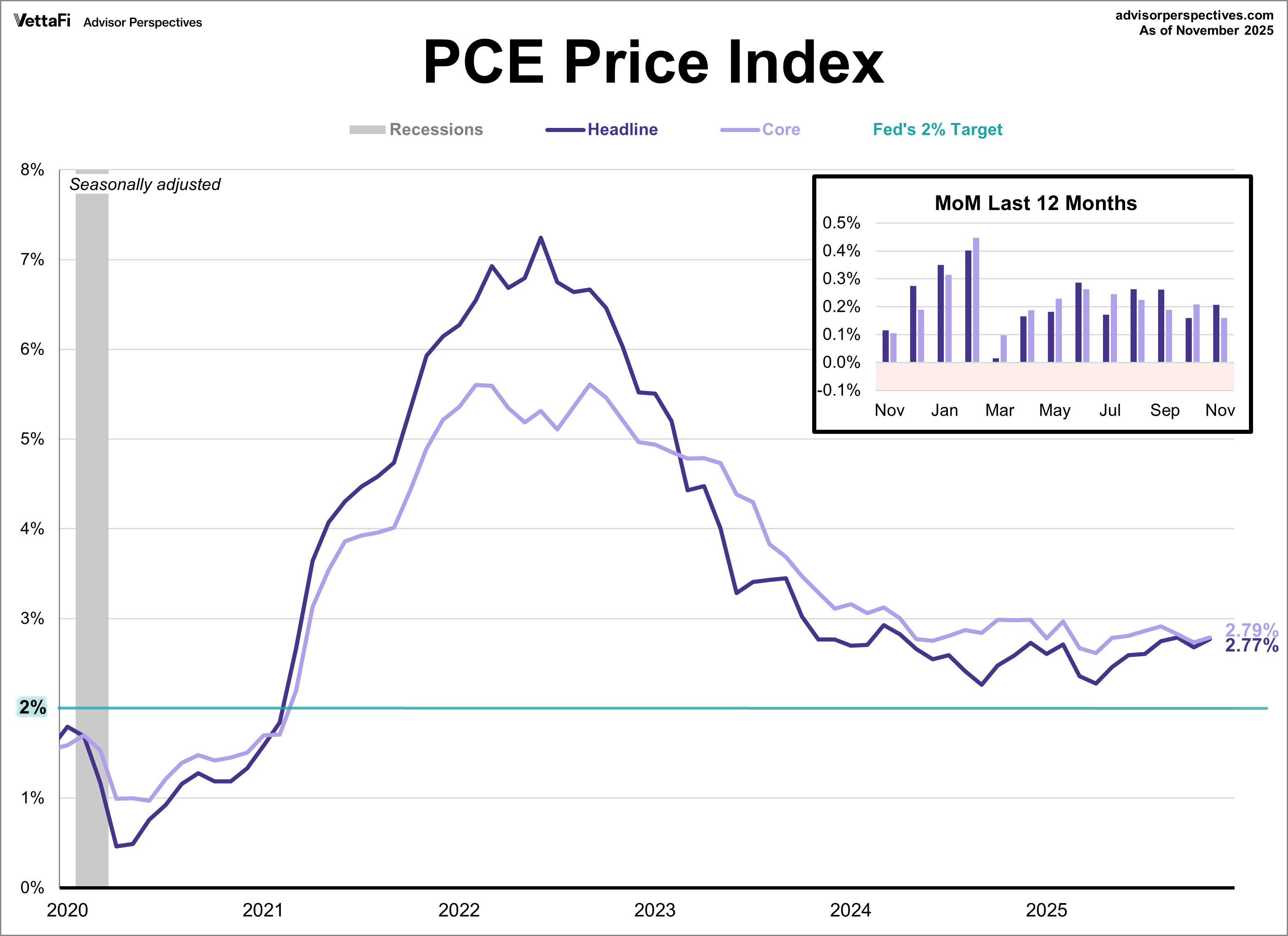

PCE Price Index

The Federal Reserve’s preferred inflation gauge showed no surprises in November, though it remains well above the 2% target. The Core Personal Consumption Expenditures (PCE) Price Index, which excludes volatile food and energy costs, rose 2.8% year-over-year in November. This was consistent with the forecast but marked a slight pickup from October. The headline index followed a similar path, rising 2.8% annually, matching expectations and ticking up slightly from the previous month. On a monthly basis, both core and headline prices increased by 0.2%, as expected.

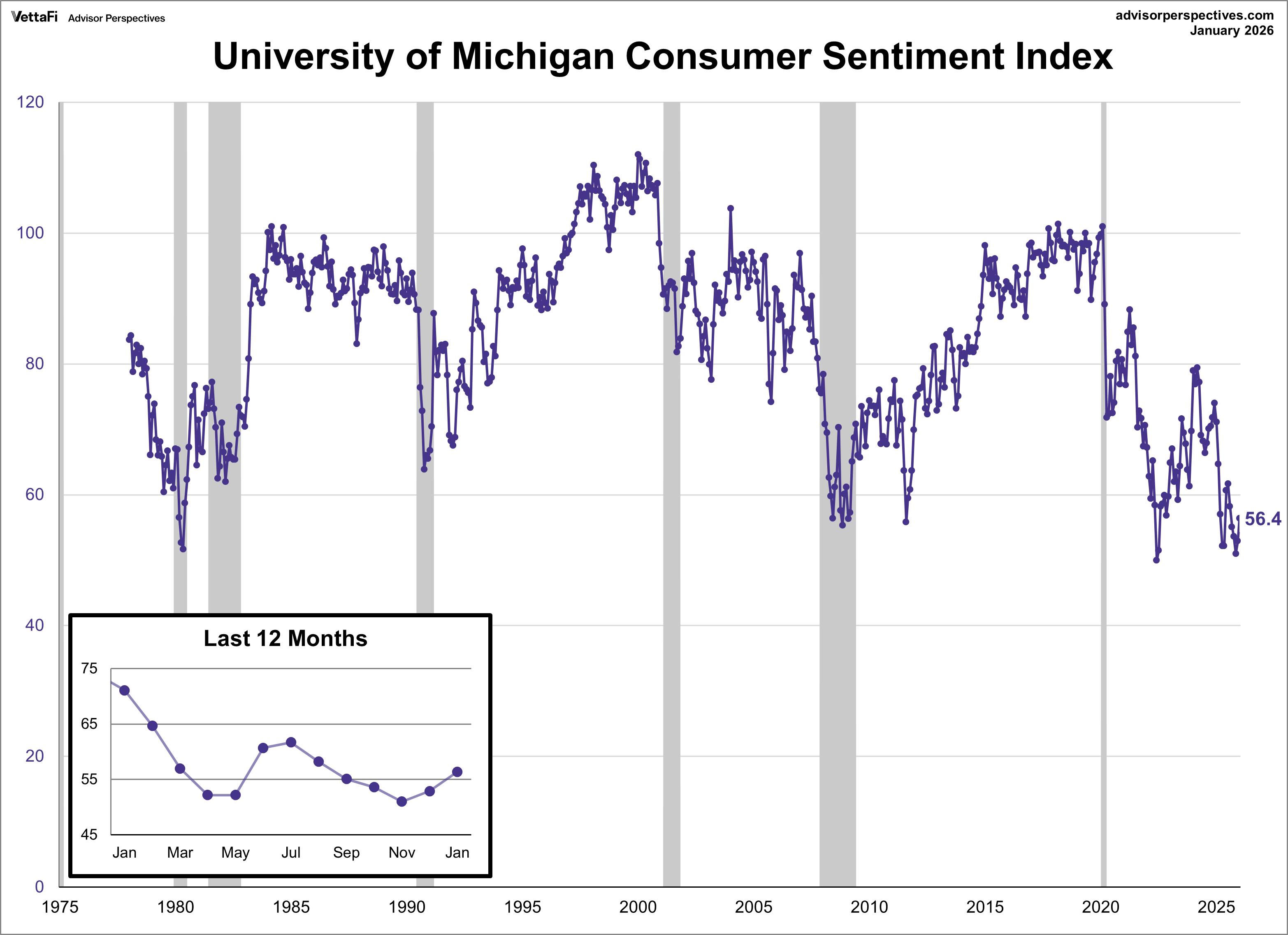

Michigan Consumer Sentiment Index

Consumer sentiment rose for a second straight month in January, reaching its highest level in five months. The University of Michigan Consumer Sentiment Index increased 3.5 points (6.6%) to 56.4 this month, exceeding the anticipated 54.0 reading. While sentiment remains over 20% below where it was a year ago, recent gains were broad-based across income levels, education, age, and political affiliation.

The “current conditions” subcomponent rose for the first time in six months, while the “expectations” subcomponents increased for a third straight month to its highest level since July. However, optimism is still tempered by ongoing price pressures and a perceived weakening in labor markets. On the inflation front, near-term expectations cooled for a fifth straight month, dropping from 4.2% in December to 4.0% in January. Long-term expectations rose for the first time in three months, inching up from 3.2% to 3.3% for the five-year outlook.

The Consumer Discretionary Select Sector SPDR ETF (XLY) is tied to consumer sentiment.

Market Reactions

The S&P 500 kicked off last week on a sour note but managed to claw back a portion of those losses, ultimately finishing the week with a loss of -0.4%. As a result, the SPDR S&P 500 ETF Trust (SPY) fell -0.4% last week. Meanwhile, the S&P Equal Weight Index was down -0.1% from the previous week and the Invesco S&P 500® Equal Weight ETF (RSP) fell -0.1%.

The 10-year Treasury yield finished the week at 4.24%, while the 2-year note finished at 3.60%.

The CME FedWatch Tool currently shows a 97% chance the Fed will hold rates steady at their meeting next week. Markets are currently pricing in two 25 basis point cuts in 2026 coming at the June and December meetings, with no additional cuts for 2027.

Economic Data in the Week Ahead

- Monday: Durable Goods Orders (Nov), Chicago Fed National Activity Index (Nov), Dallas Fed Manufacturing Index (Jan)

- Tuesday: S&P/Case-Shiller Home Price Index (Nov), FHFA Home Price Index (Nov), Conference Board Consumer Confidence Index (Jan), Richmond Fed Manufacturing Index (Jan)

- Wednesday: FOMC Meeting

- Thursday: Weekly Jobless Claims, Trade Balance (Nov)

- Friday: Producer Price index (Dec), Chicago PMI (Jan)