{kind=link}

While recent market performance reflects optimism over potential geopolitical de-escalation, underlying economic data reveals a complex landscape of intensifying price pressures and cooling growth. Consumer inflation has surged to a near two-year high, driven by a spike in energy costs, even as the broader economy shows signs of losing momentum. Amidst record-low consumer sentiment and shifting inflation expectations, the Federal Reserve faces a critical juncture in balancing price stability with a softening GDP.

Inflation: Energy Costs Drive Price Surges

Consumer Price Index

Consumer inflation climbed to its highest level in nearly two years, with the Consumer Price Index (CPI) reaching 3.3% in March. While this was a sharp acceleration from February’s 2.4%, it landed slightly below the 3.4% forecast .On a monthly basis, prices were up 0.9%, less than the expected 1.0% growth but still marking the largest monthly gain since 2022. The spike was driven by a significant increase in energy costs tied to the Iran conflict. Specifically, the gasoline index was up over 21%, its largest monthly increase on record and accounting for almost 75% of the index’s total gain.

Core inflation, which excludes volatile food and energy, rose more modestly, moving from 2.5% in February to 2.6%. Additionally, core prices were up 0.2% from the previous month. Both figures came in just below their respective forecasts of 2.7% and 0.3%.

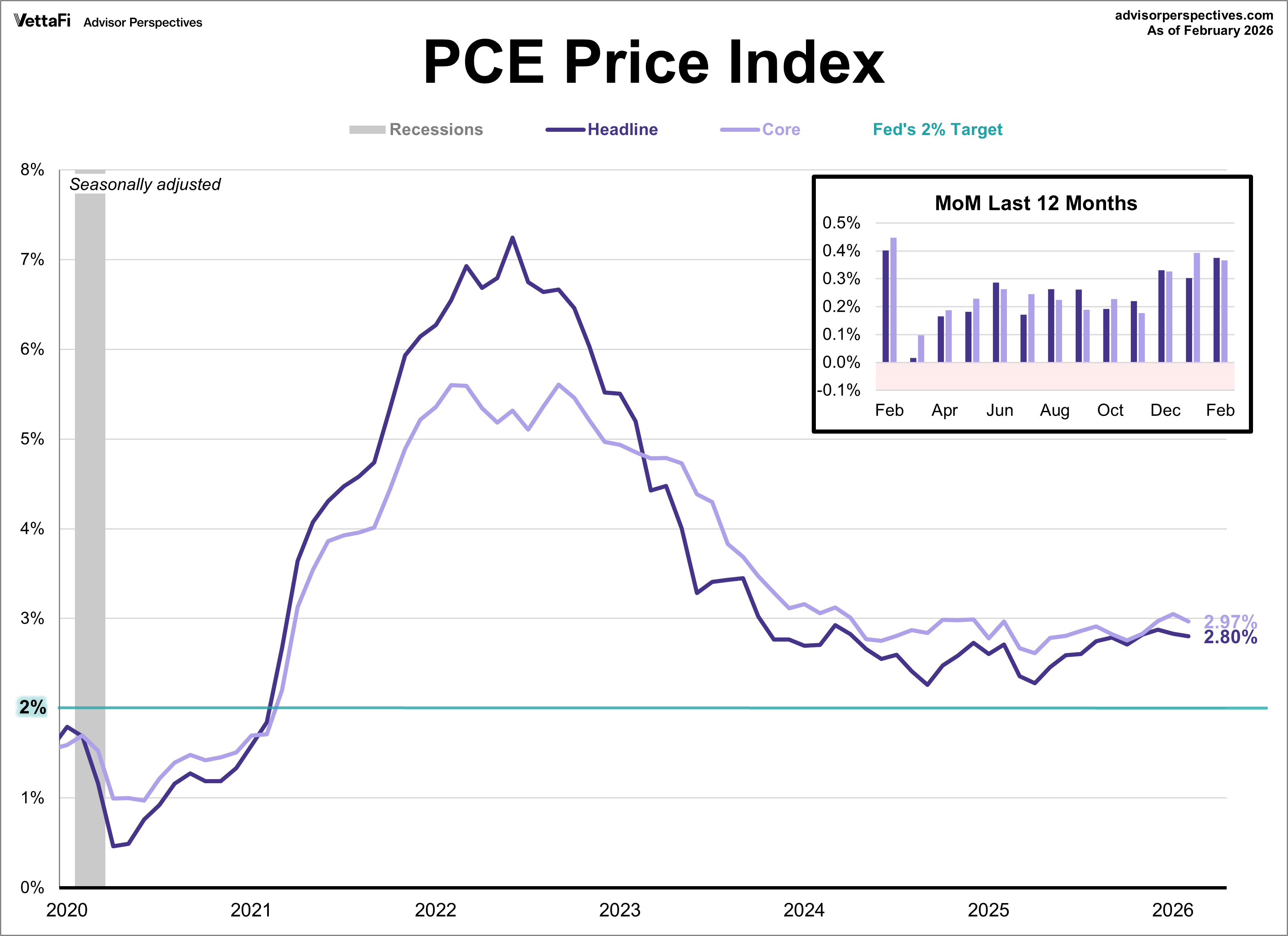

PCE Price Index

The Federal Reserve’s preferred inflation gauge, the Core Personal Consumption Expenditures (PCE) Price Index, revealed that inflation was already heating up prior to the recent conflict. The delayed data shows the Core PCE Index rose 3.0% year-over-year in February, remaining well above the Fed’s target. This core figure, which strips out volatile food and energy costs, matched expectations and slowed slightly from January’s 3.1% reading. The headline PCE index followed a similar trajectory, increasing 2.8% annually, which matched both the prior month’s data and expectations. On a monthly basis, both core and headline prices climbed 0.4%, marking the sharpest monthly increase in a year. This underlying momentum, combined with the conflict’s immediate effect on energy prices and March’s CPI reading, suggests inflation is expected to jump sharply in March as gas prices have surged beyond $4.

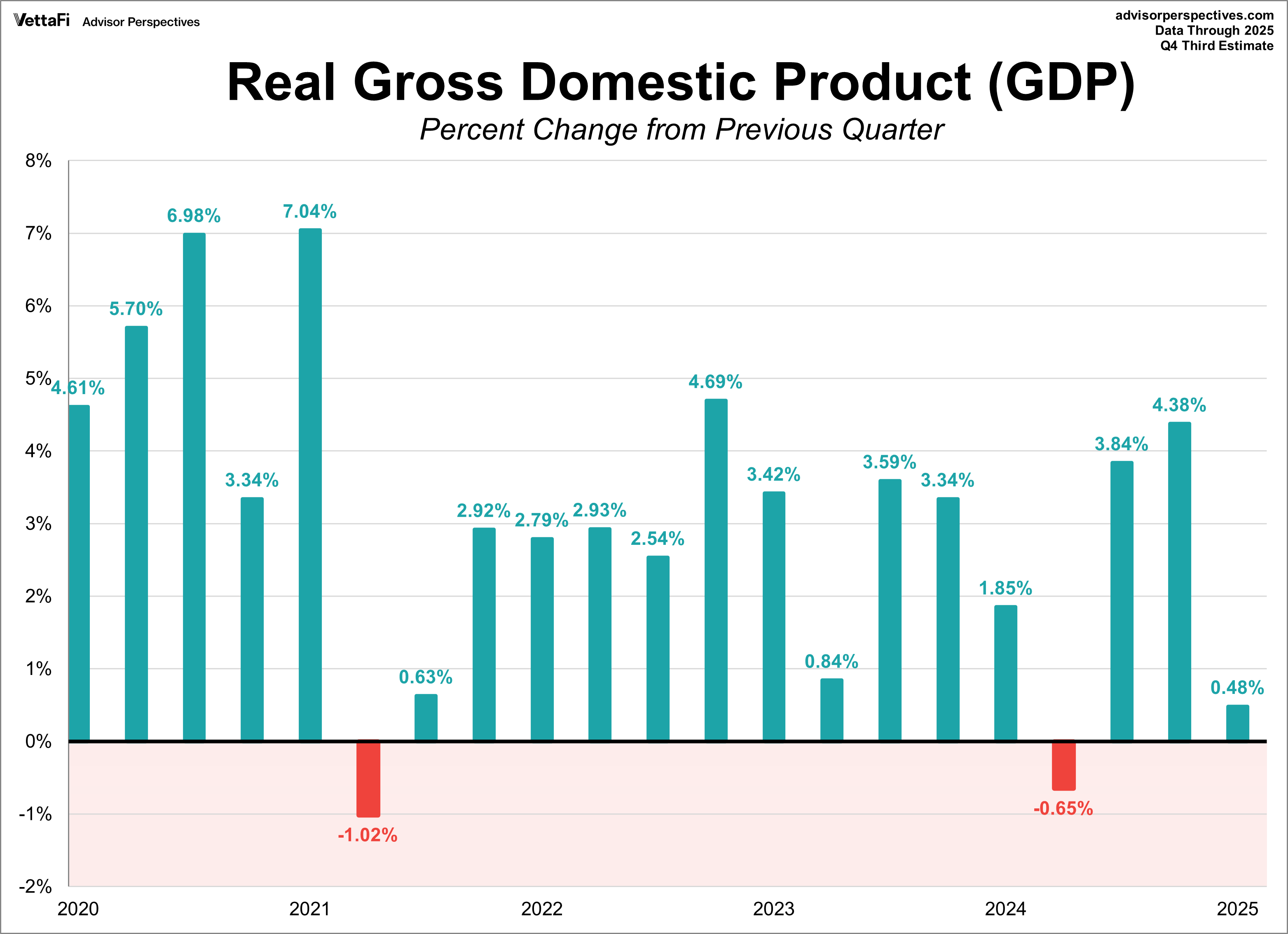

Economic Growth: GDP Momentum Fades

The U.S. economy lost significant momentum in the final months of 2025, according to the BEA. Real GDP expanded at an annual rate of 0.5% in the fourth quarter, a sharp declaration from the robust 4.4% growth recorded in the third quarter and lower than the previous 0.7% forecast. While the expansion was primarily driven by increases in consumer spending and business investment, these gains were partially offset by notable declines in exports and government spending.

Consumer Outlook: Sentiment Hits Record Lows

Consumer sentiment plunged nearly 11% to its lowest level on record, a decline driven largely by the outbreak of the Iran conflict. However, it’s important to note that the majority of interviews were completed prior to the announcement of a temporary ceasefire. The Michigan Consumer Sentiment Index dropped 5.7 points to 47.6, missing the forecast of 51.6, as consumers cited geopolitical instability and rising gas prices for their increased pessimism.

This month’s drop was widespread, affecting all age groups, income levels, and political affiliations. Both short-term and long-term expectations dropped to historic lows but the director of the survey noted that expectations will likely improve with the conclusion of the conflict and moderating gas prices.

Regarding inflation, near-term expectations jumped from 3.8% in March to 4.8%, the largest single month increase since last April when tariffs were announced. In the long-term, five-year expectations rose from 3.2% in March to 3.4%, the highest level since November.

The Consumer Discretionary Select Sector SPDR ETF (XLY) is tied to consumer sentiment.

Market expectations, as reflected by the CME FedWatch Tool, strongly favor the Federal Reserve holding interest rates steady at their upcoming meeting, with a 98% probability versus a 2% chance of a 25 basis point increase. Current market pricing suggests a stable rate environment will persist throughout 2026, followed by two anticipated 25 basis point rate cuts in 2027.