{kind=link}

The U.S. economy faced intensifying headwinds in May as both consumer and wholesale inflation metrics surged to multi-year highs. Driven largely by accelerating energy and supply chain costs, these dual jumps signal persistent upward price pressures that threaten to keep household expenses elevated. While consumer sentiment managed a minor uptick in the preliminary June reading, the overall outlook remains bleak as consumers continue to grapple with rising prices.

Key Takeaways

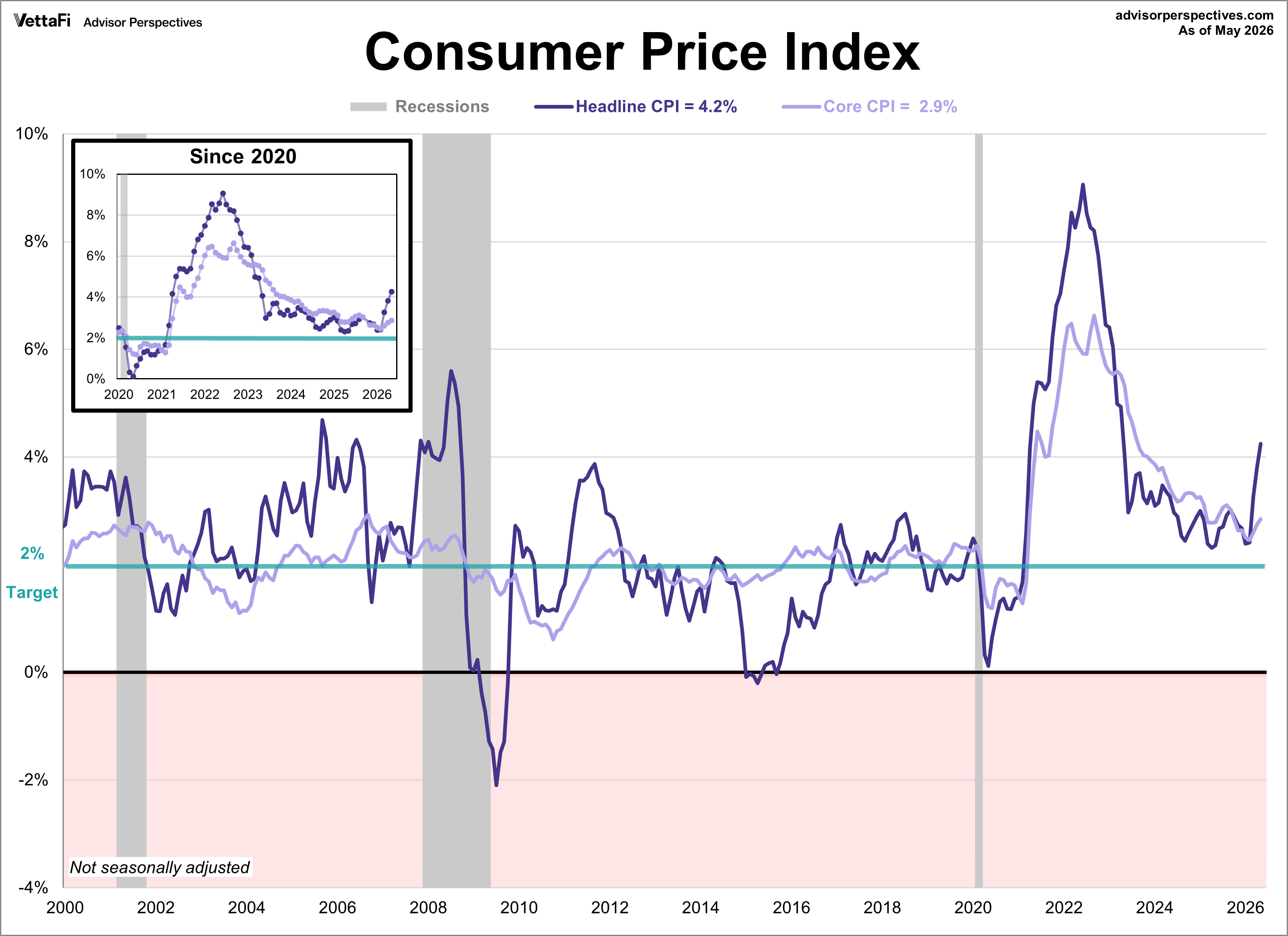

- The Consumer Price Index (CPI) reached a three-year high of 4.2% in May, fueled by a 0.5% monthly price increase where energy costs alone accounted for over 60% of the total growth.

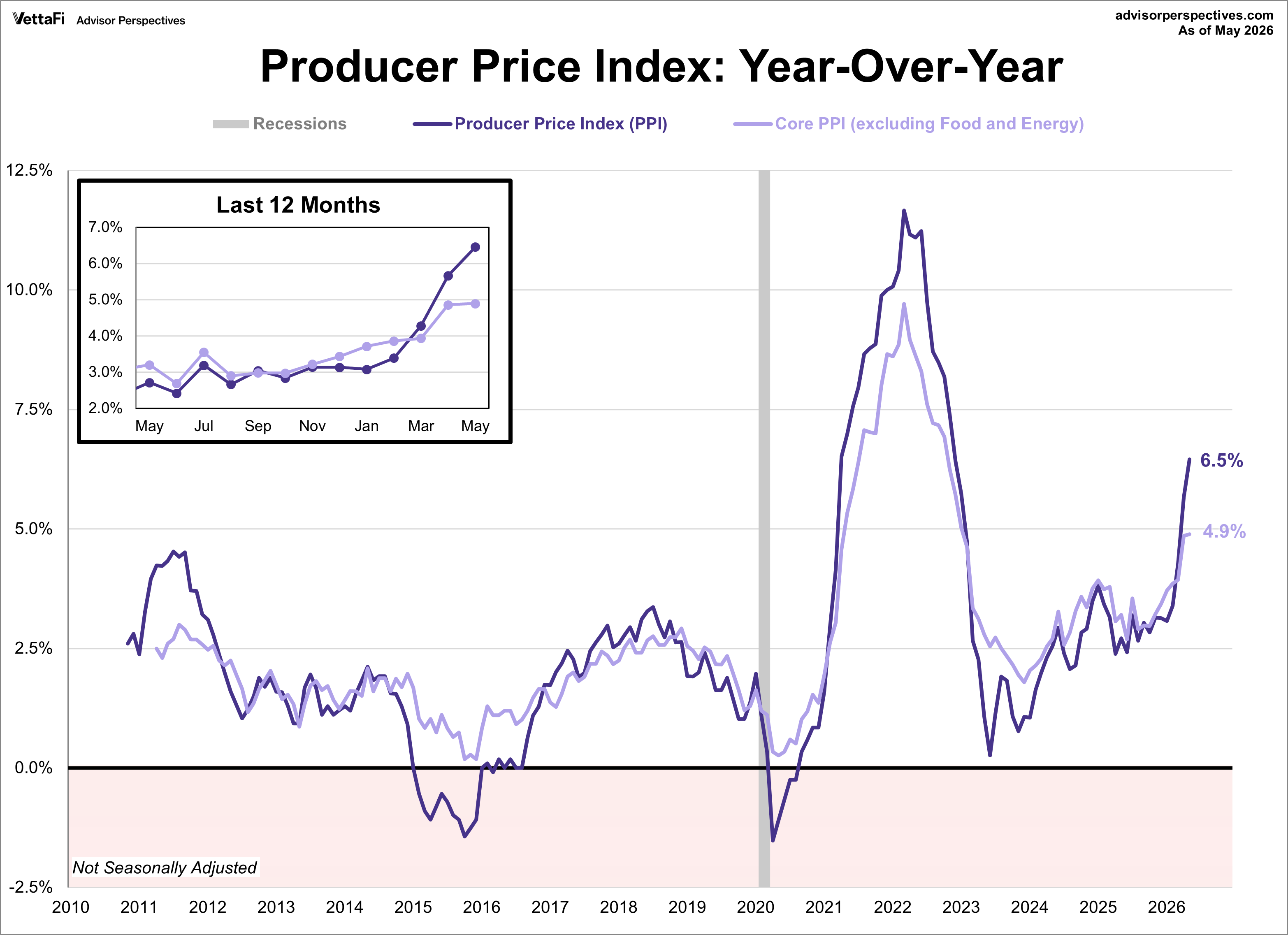

- The Producer Price Index (PPI) accelerated to a multi-year high of 6.5% in May, driven by a 1.1% monthly jump that exceeded the 0.7% forecast.

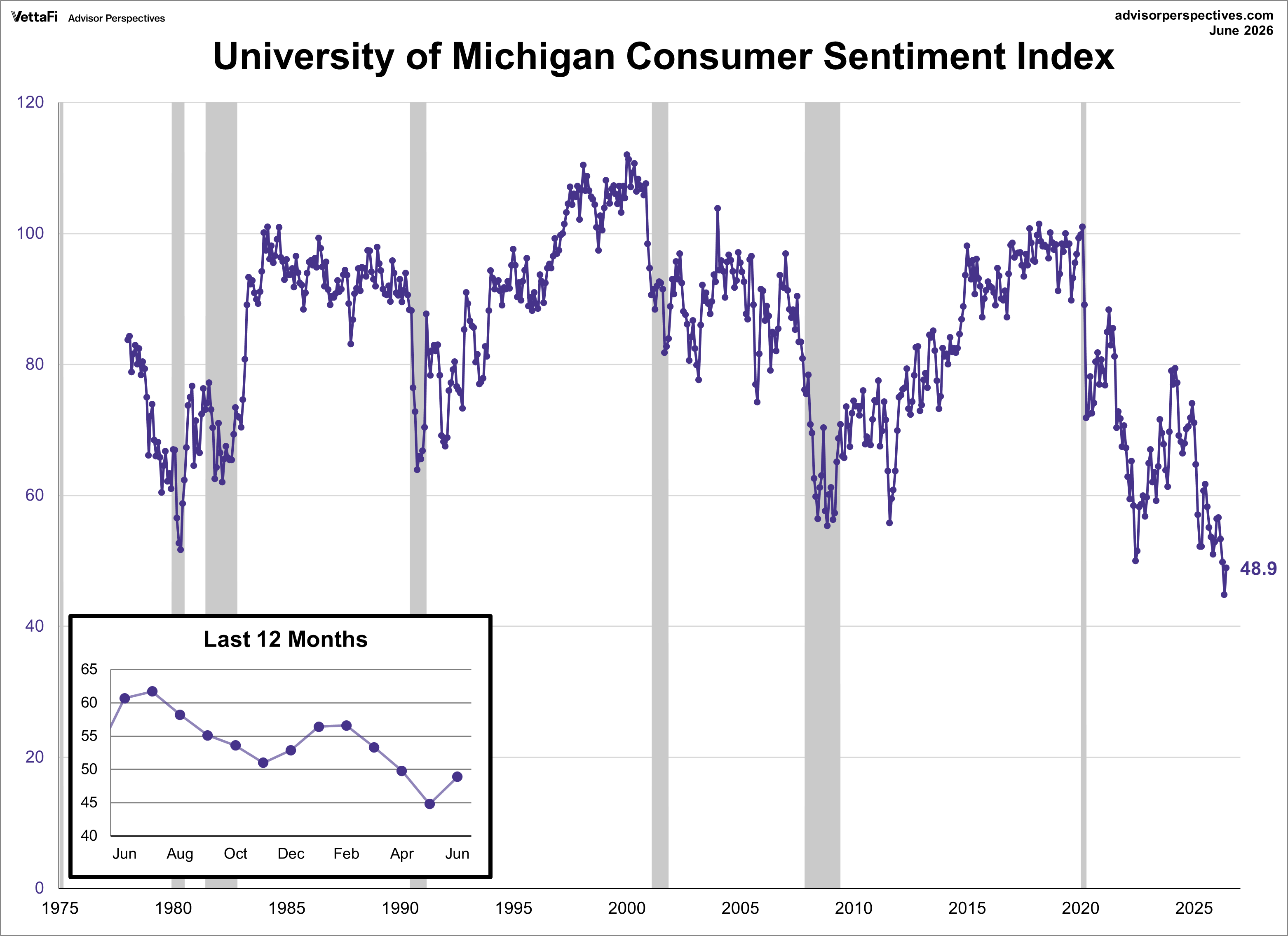

- The Michigan Consumer Sentiment Index rose 9% in June to 48.4, breaking a four-month decline and coinciding with a drop in one-year and five-year inflation expectations to 4.6% and 3.5%, respectively.

Consumer Price Index: Energy Costs Drive Inflation to 3-Year High

Consumer inflation surged to its highest level in over three years in May, with the Consumer Price Index reaching 4.2% year-over-year. This marks a sharp acceleration from April’s 3.8% reading, though it was consistent with the forecast. On a monthly basis, prices rose 0.5% as expected. Once again, the jump was led by energy, shelter, and food, with energy alone accounting for over 60% of the total increase.

Core inflation, which excludes volatile food and energy prices, showed more moderation last month but still crept upward. The core CPI rose from 2.8% in April to 2.9%, marking its highest level since last September and in line with expectations. Additionally, core prices were up 0.2% from the previous month, coming in just below the projected 0.3% growth.

Wholesale Inflation Warning: Hot PPI Data Delivers Setback

Delivering a further setback to the broader inflation outlook, wholesale prices came in hotter than expected in May. The Producer Price Index (PPI) accelerated to 6.5% annually, a significant acceleration from April’s 5.7% and marking its highest level since November 2022. On a monthly basis, prices jumped 1.1%, well above the projected 0.7% increase.

Similar to consumer inflation, this upward pressure was largely concentrated in volatile sectors like food and energy. Consequently, core PPI rose a milder 0.4% last month and 4.9% annually, with both metrics coming in below their respective forecasts of 0.5% and 5.4%.

Because producers often pass rising overhead costs directly to the public, the continued spike in the headline PPI serves as a warning sign that consumer-level inflation may continue to heat up in the months ahead.

Inflation Concerns Keep Consumer Sentiment Near Historic Lows

While consumer sentiment improved for the first time in four months in June, it remains historically low as ongoing inflation concerns continue to burden households. The preliminary reading of the Michigan Consumer Sentiment Index came in at 48.4, marking a 9% increase from May’s record low and exceeding the forecast of 46.1. The uptick in sentiment was broad-based across various demographics, including age, education, political affiliation, and income.

Market Reactions and Fed Outlook

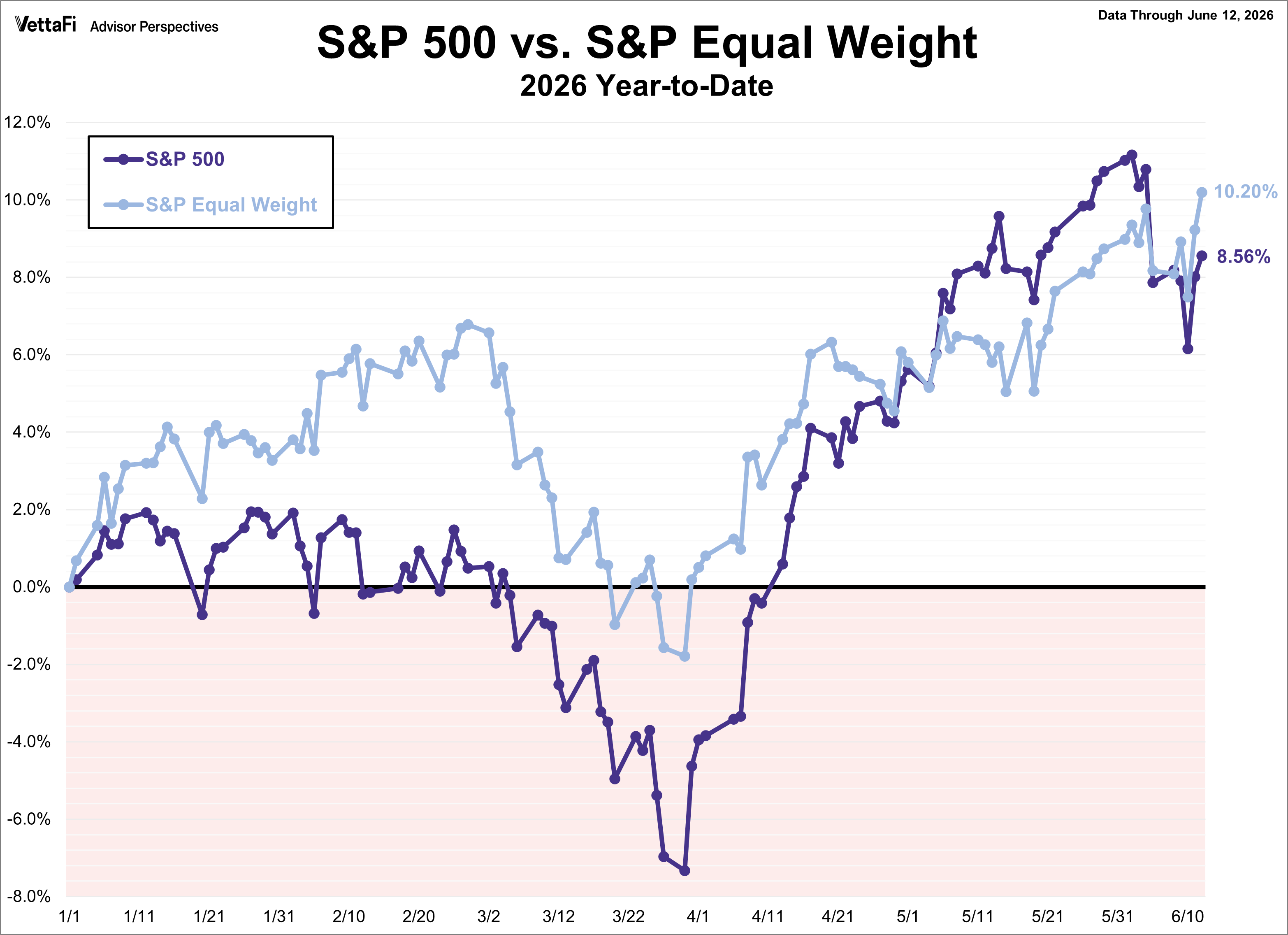

The S&P 500 shook off a rocky start last week, rallying in the back half to secure a 0.6% weekly gain. The turnaround was anchored by a massive 1.8% surge on Thursday, which marked the index’s best single-day performance in over two months. As a result, the SPDR S&P 500 ETF Trust (SPY) rose 0.6% last week. Meanwhile, the S&P Equal Weight Index was up 1.9% from the previous week and the Invesco S&P 500® Equal Weight ETF (RSP) rose 1.9%.

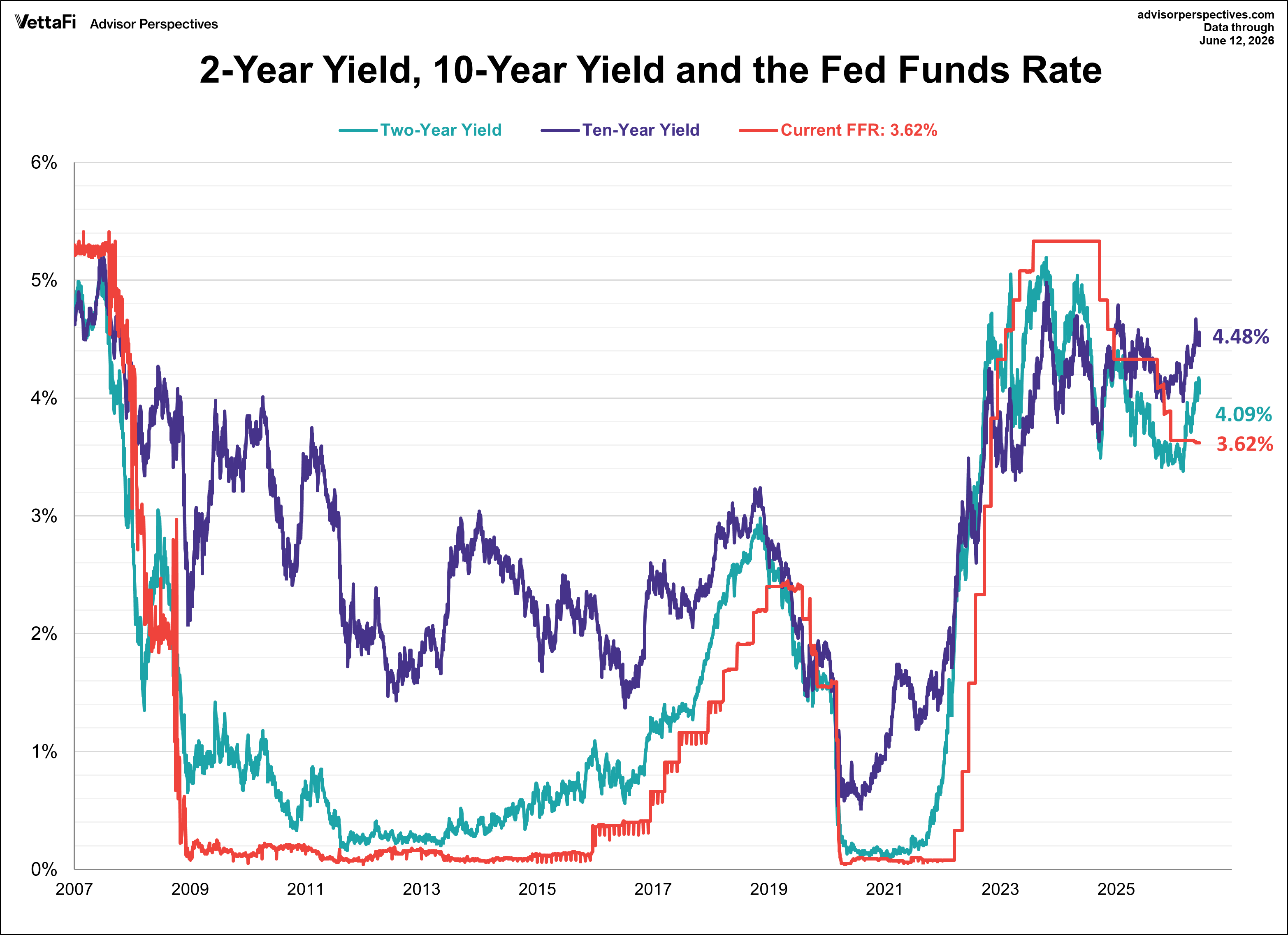

The 10-year Treasury yield finished the week at 4.48%, while the 2-year note finished at 4.09%.

The CME FedWatch Tool currently shows a 96% likelihood that the Federal Reserve will hold rates steady at its meeting this week, versus a 4% chance of a cut. Markets are currently pricing in a 25 basis point hike by the end of 2026 followed by a pause through all of next year.

Looking Ahead: Economic Data for the Week of June 15, 2026

- Monday: Empire State Manufacturing Index (June), Industrial Production (May), NAHB Housing Market Index (June)

- Tuesday: Housing Starts (May), Building Permits (May)

- Wednesday: Retail Sales (May), Pending Home Sales (May), Fed Interest Rate Decision

- Thursday: Weekly Jobless Claims, Philadelphia Fed Manufacturing Index (June)

- Friday: U.S. Holiday