{kind=link}

State Street Investment Management recently released its Midyear Outlook, and it captured the market’s moment incredibly well, depicting an environment marked by both resilience and fragility.

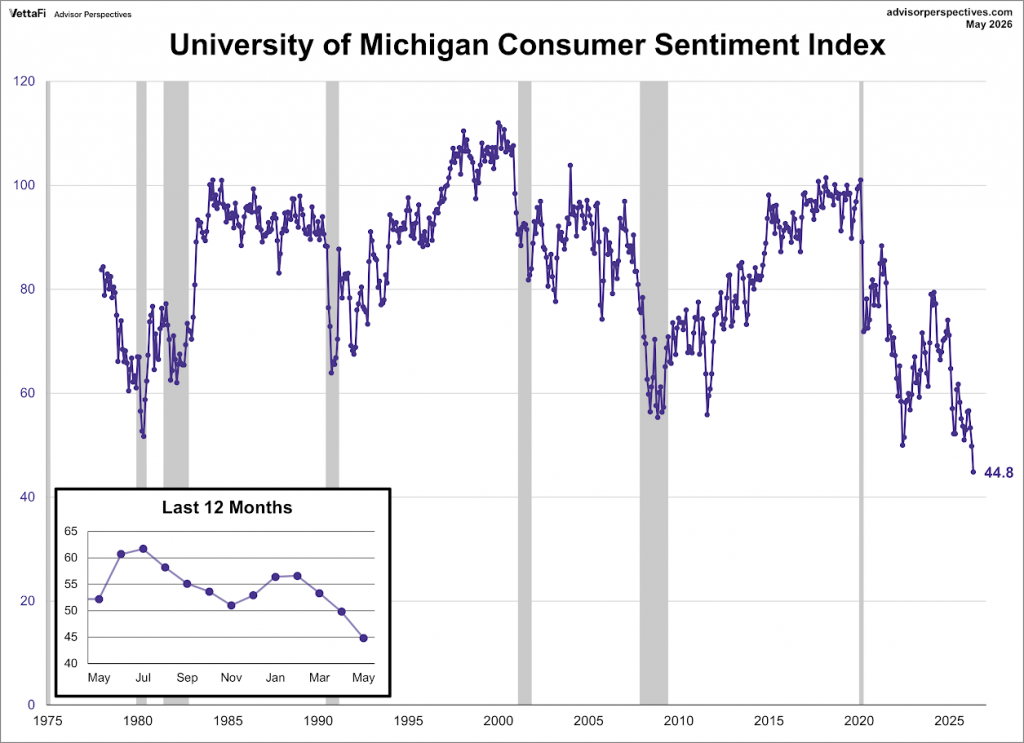

When we dive into the latest macro economic data, we see exactly that: a market that’s anchored on solid fundamentals but that’s also growing fragile as confidence wanes. Strong earnings results and economic expansion (US GDP increased at 2% annualized vs. 0.5% in Q4 2025) stand in contrast to rising inflation and plummeting consumer sentiment, now at record lows.

To put this dichotomy in pictures, consider some numbers:

Source:FactSet

VERSUS

Source: Advisor Perspectives

Source: Advisor Perspectives

The bull market keeps marching on, defiant, but the call for sharper risk management grows louder as correlations — the traditional diversification mechanism in portfolios — become unreliable.

These are interesting times indeed.

Demand Across the Board

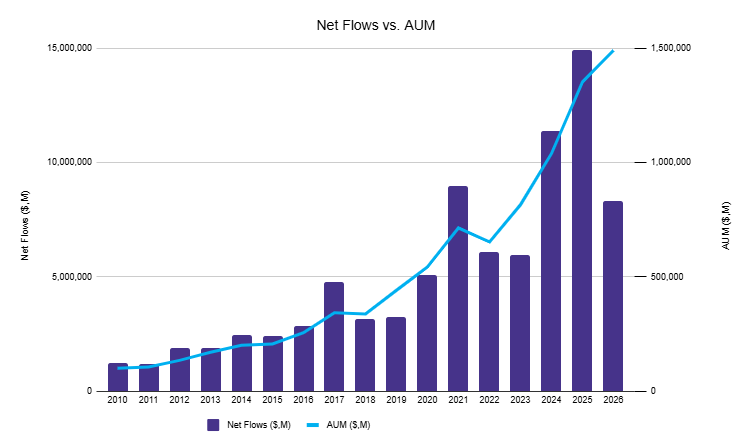

A look at ETF asset flows through June 1 shows that investors are paying attention. They have not only been relying heavily on the efficiency, accessibility, and flexibility of the ETF wrapper to navigate these macro conditions, but they’ve been adjusting asset allocation and portfolio positioning across strategy types.

Source: VettaFi (2026 flows and AUM data as of June 1)

Source: VettaFi (2026 flows and AUM data as of June 1)

Year-to-date, every asset class is net positive in asset gathering. From equities to bonds to real assets to derivatives, investors have embraced it all. Of the record $832 billion in net ETF creations so far in 2026, equities have snagged 64% of the flows, fixed income a whopping 32%, and alternatives/commodities sit with a 4% haul.

Among the most popular ETFs this year are index-based low-cost equity core giants like the Vanguard S&P 500 ETF (VOO) and the State Street SPDR Portfolio S&P 500 ETF (SPYM), with combined inflows of more than $100 billion. Appetite for U.S equity remains robust as corporate fundamentals stay strong.

Income, too, has been a massive theme. Cash-management favorites like the ProShares GENIUS Money Market ETF (IQMM) and the iShares 0-3 Month Treasury Bond ETF (SGOV) have captured a massive $43 billion in combined net inflows. Fixed income ETFs are punching well above the relative-asset weight this year.

Thematic portfolios honed in on the latest opportunity set like the Roundhill Memory ETF (DRAM) are seeing blockbuster demand. AI-related portfolios of all shapes and sizes continue to resonate as the theme evolves.

The SPDR Gold Minishares Trust (GLDM) continues to rake in net new money even though gold is up only about 3% this year; metals and real assets ETFs are finding a lot of traction, too.

The iShares Bitcoin Trust ETF (IBIT) and the NEOS Bitcoin High Income ETF (BTCI) are leading crypto-related demand, while the Capital Group Core Balanced ETF (CGBL) and the State Street Bridgewater All Weather ETF (ALLW) lead flows in the asset allocation ETF category.

The diverse list of popular ETF solutions answering the call to participate-but-diversify goes on.

Positioning for What’s Ahead

To quote SSIM, it’s important to note that “markets are bending — not breaking” and that investing for what comes next may demand broader thinking as globalization gives way to national security themes, and “potentially higher interest rates, sticky inflation, and lower corporate profit margins” demand strategic thinking.

“The bull market may endure, but without meaningful changes to investment portfolios, investors may be unprepared for what comes next,” SSIM said in the outlook.

The asset manager’s big midyear call is to lean into the path to diversification, seeking exposure to different tiers of market capitalization, taking a hands-on approach to interest and credit risks, and turning to real assets and multi-asset portfolios for broader diversification.

“The foundation for the multiyear bull market remains intact,” the firm said. “If the economy and earnings continue to grow, stocks may continue to outpace inflation over time. But the evolving shift from the efficiency of globalization to the resilience of deglobalization requires thoughtful adjustments to diversified investment portfolios.”

More of the Same, Just Louder

Diversification isn’t a new theme. In fact, it’s been a widely used call to action for the past several months as asset managers and investors alike worry about global macro conditions, geopolitical noise, and market concentration even in the face of strong corporate fundamentals and economic growth.

Midyear outlooks now emerging as we near the second half of the year aren’t preaching anything new. But they are reinforcing a call that has worked, and one that ETF investors seem to be increasingly embracing.

For more news, information, and strategy, visit the ETF Strategist Content Hub.