{kind=link}

Last week’s economic data was defined by conflicting signals from the consumer. While retail figures suggest resilience, sentiment levels have plummeted to record lows. Meanwhile, the S&P 500 continued its historic rally as markets prepare for the upcoming Fed decision.

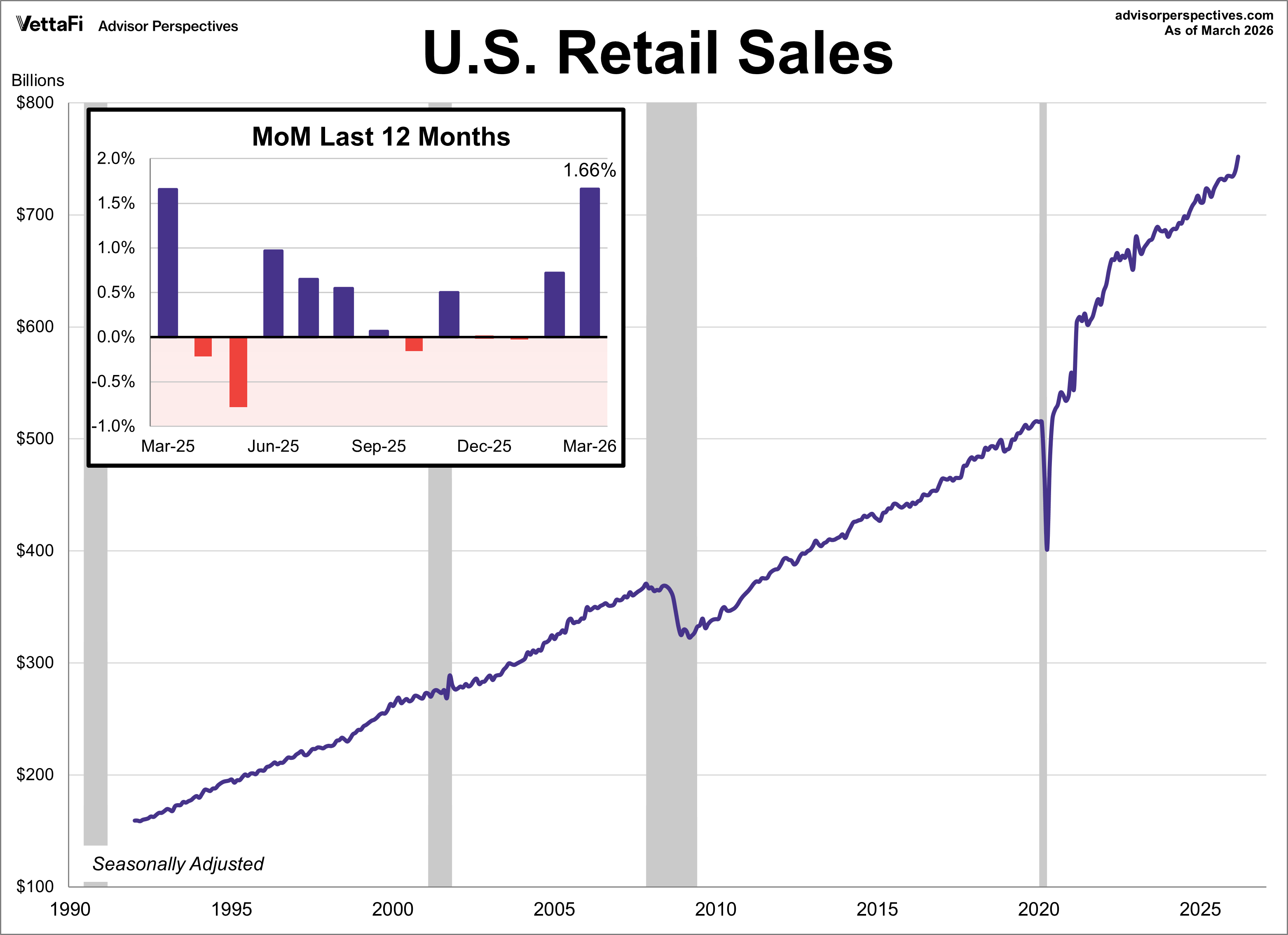

Retail Sales: Gas Purchases Drives Spending Surge

Consumer spending was more robust than expected in March as headline retail sales surged 1.7%, sharply outpacing the projected 1.4% growth and marking the largest monthly increase since early 2023. Core sales, which exclude autos, also outperformed expectations at 1.9% against a 1.4% forecast. However, these figures were heavily skewed by a 15.5% record spike in gas purchases following the escalation of the Iran conflict. Since retail data is not adjusted for price changes, much of this “growth” reflects the record cost of fuel rather than actual consumer volume. Consequently, control purchases, which strip out the noise of gasoline, autos, and building materials, rose a more modest 0.8%, providing a far more reliable reading of the underlying economy despite still beating the modest 0.2% projection.

Retail sales could impact the SPDR S&P Retail ETF (XRT), VanEck Retail ETF (RTH), Amplify Online Retail ETF (IBUY), and ProShares Online Retail ETF (ONLN).

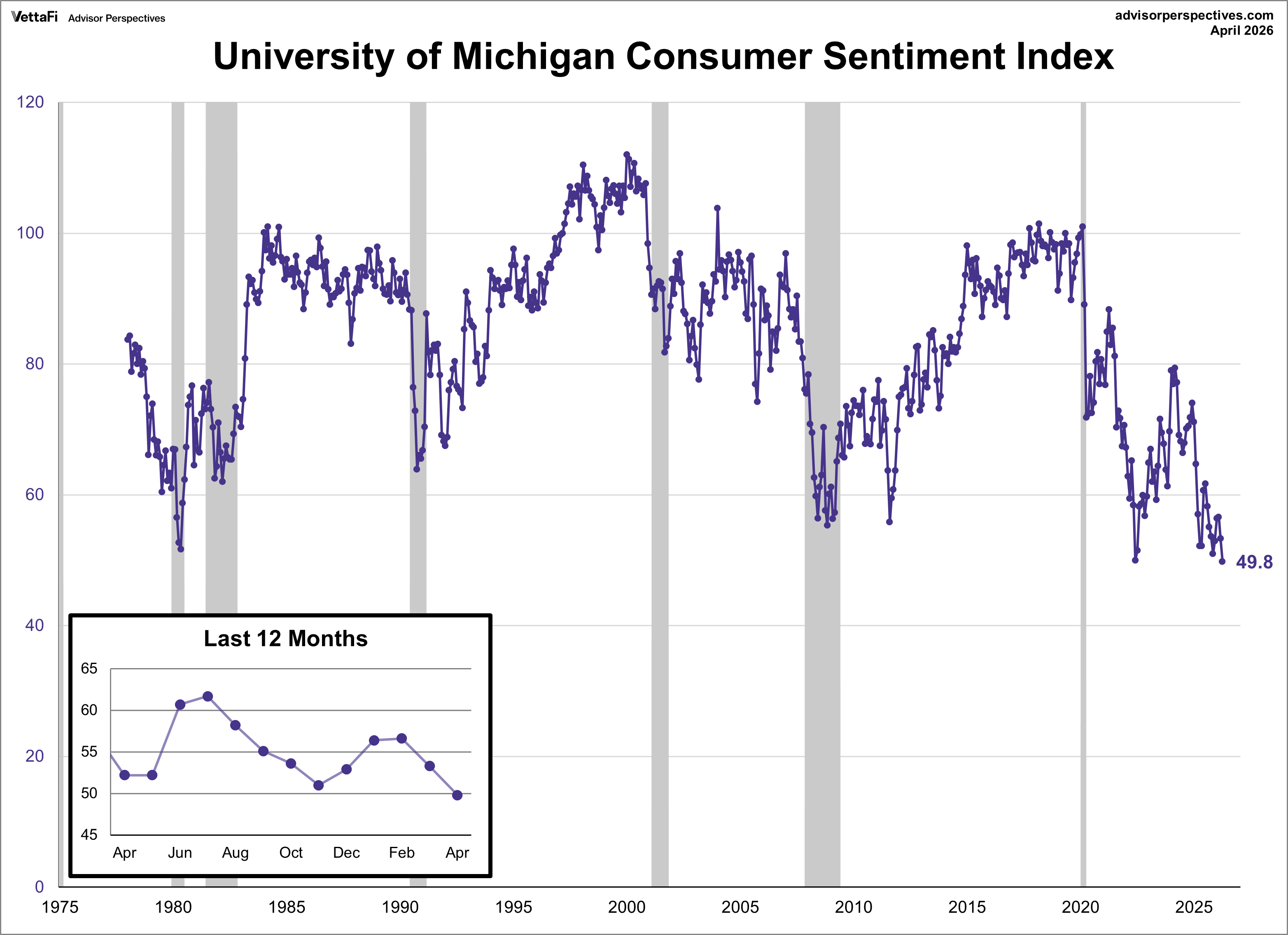

Consumer Outlook: Sentiment Hits Record Lows

Consumer sentiment in April hit its lowest recorded level, largely attributed to the ongoing Iran conflict, despite a modest late-month rise. The final reading of the Michigan Consumer Sentiment Index was 49.8, surpassing the initial forecast of 47.6. However, this still represents a 3.5-point decline from March, as inflation and price shocks continue to pressure consumers.

The drop in sentiment was broad-based, impacting all demographics including age groups, education levels, income levels, and political affiliations. Both short- and long-term expectations fell to their lowest points this year. Inflation expectations saw a notable increase with near-term expectations jumping from 3.8% in March to 4.7%, the largest one-month rise since tariffs were announced last April. Long-term (five-year) expectations also rose, moving from 3.2% in March to 3.5%, the highest level since October.

The Consumer Discretionary Select Sector SPDR ETF (XLY) is tied to consumer sentiment.

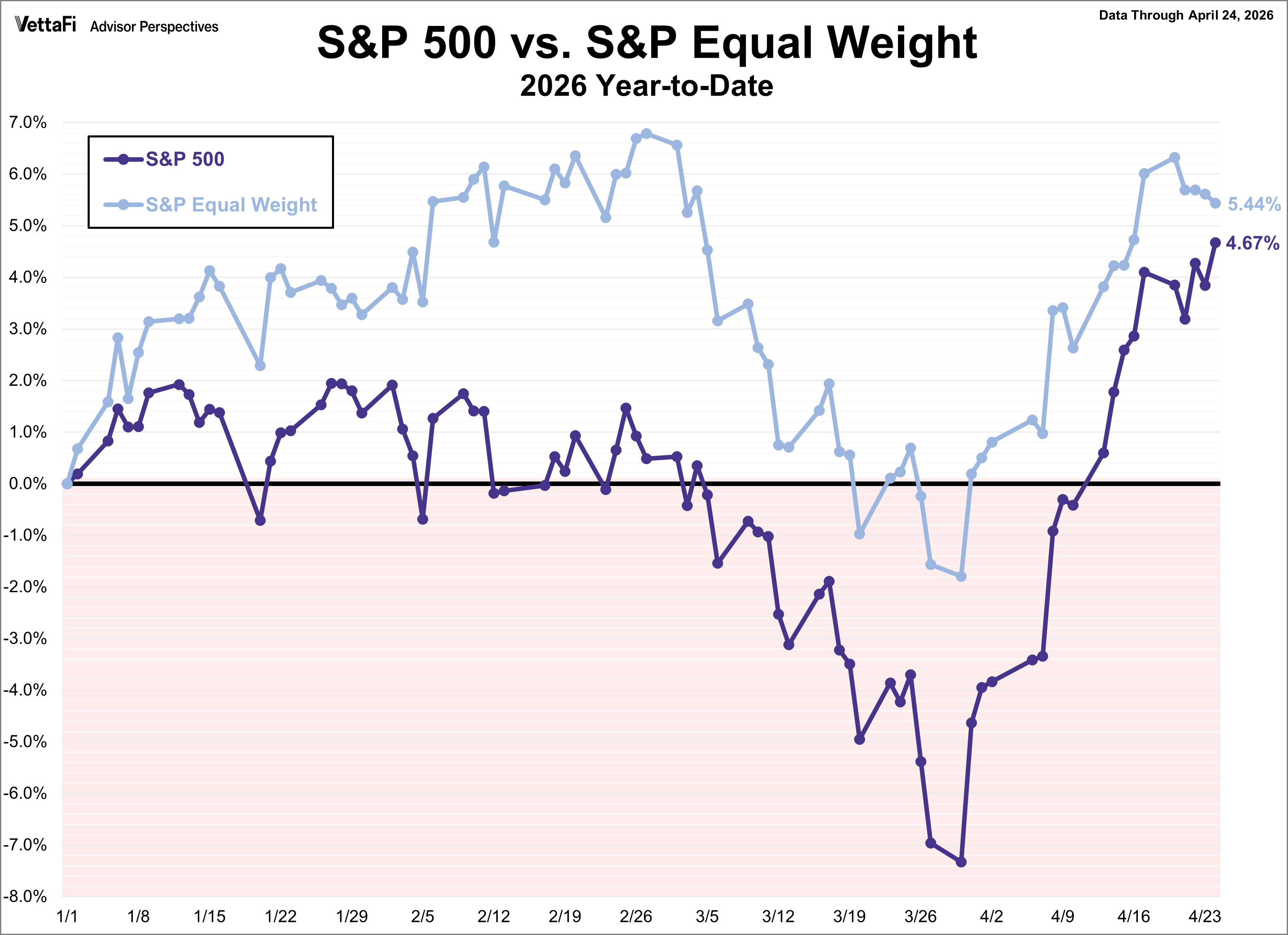

Market Reactions

The S&P 500 capped off last week with a fresh record high, finishing up 0.5%. This marks the fourth consecutive winning week for the index, its longest streak since late 2024. As a result, the SPDR S&P 500 ETF Trust (SPY) rose 0.5% last week. Meanwhile, the S&P Equal Weight Index was down 0.5% from the previous week and the Invesco S&P 500® Equal Weight ETF (RSP) fell 0.5%.

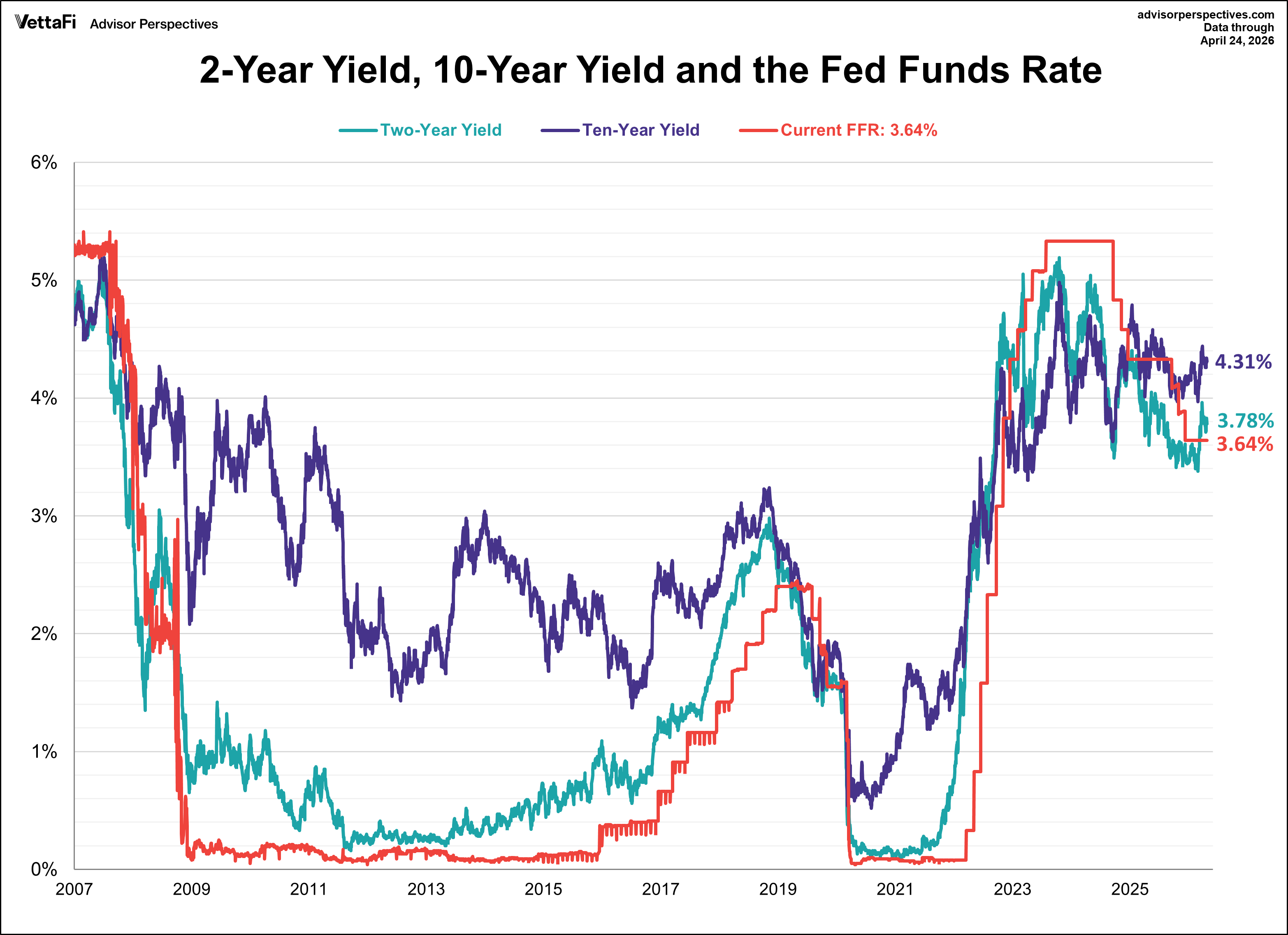

The 10-year Treasury yield finished the week at 4.31%, while the 2-year note finished at 3.78%.

The Fed is expected to maintain current interest rates this week, with the CME FedWatch Tool indicating a near 100% probability. Market expectations show no further rate adjustments, either cuts or hikes, or the remainder of 2026. In 2027, two 25 basis point rate cuts are currently anticipated at the end of the year.

- Monday: Dallas Fed Manufacturing Index (Apr)

- Tuesday: S&P Cotality Case-Shiller Home Price Index (Feb), FHFA House Price index (Feb), Conference Board Consumer Confidence Index (Apr), Richmond Fed Manufacturing Index (Apr), Home Ownership Rate (Q1 2026)

- Wednesday: Fed Interest Rate Decision, Durable Goods (Mar), Housing Starts (Mar), Building Permits (Mar)

- Thursday: Weekly Jobless Claims, Gross Domestic Product (Q1 2026 Advance Estimate), PCE Price Index (Mar), Personal Income (Mar), Chicago PMI (Apr)

- Friday: S&P Global Manufacturing PMI (Apr), ISM Manufacturing PMI (Apr)

Originally published on Advisor Perspectives

For more news, information, and strategy, visit ETF Trends.