{kind=link}

This article provides an update on the monthly moving averages we track for the S&P 500 and the Ivy Portfolio after the close of the last business day of the month.

The Ivy Portfolio

The Ivy Portfolio is based on the asset allocation strategy used by endowment funds from Harvard and Yale. It is an equally weighted portfolio constructed with 5 ETFs that feature a mix of different asset classes. By allocating across different asset classes, diversification is achieved, and risk is reduced. The different asset classes and their corresponding ETFs are below.

- Domestic stocks, represented by Vanguard Total Stock Market ETF (VTI)

- International stocks, represented by Vanguard FTSE All-World ex-US Index Fund (VEU)

- Bonds, represented by iShares 7-10 Year Treasury Bond ETF (IEF)

- Real estate, represented by Vanguard Real Estate ETF (VNQ)

- Commodities, represented by Invesco DB Commodity Index Tracking Fund (DBC)

The process of using the Ivy Portfolio is quite simple. First, compose a diversified portfolio from each of the major asset classes held in equal weight (see above). Then, compute a moving average of closing prices over the prior 10 months for each fund (or desired time frame). Lastly, observe the portfolio at the end of each month. If a fund closes out the month below the level of its moving average, sell it and hold cash, repurchasing only when it closes back above its moving average at the end of any subsequent month. Similarly, if a fund closes out the month above the moving average, hold it.

For a fascinating analysis of the Ivy portfolio strategy, see this article by Adam Butler, Mike Philbrick, and Rodrigo Gordillo: Faber’s Ivy Portfolio: As Simple as Possible, But No Simpler.

The Ivy Portfolio: Latest Data

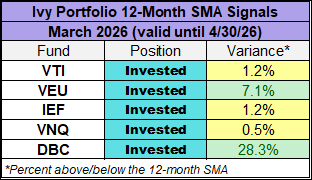

The table below details the 10-month simple moving average (SMA) for the five Ivy Portfolio asset classes. As of month-end March, the signal has shifted: while all funds were in ‘invest’ positions in February, two have now crossed into ‘cash.’ Specifically, VTI and VNQ closed below their 10-month SMA, leaving only three funds with active ‘invest’ signals.

To assist with trend monitoring, the table also includes the percentage by which each fund sits above or below its moving average. Positions highlighted in yellow indicate a fund is within 2% of its signal, flagging a potential reversal in the coming month.

For a broader perspective, the following table displays the 12-month simple moving average (SMA) signals. Unlike the 10-month indicators, the 12-month signals remain robust; as of month-end March, all five Ivy Portfolio ETFs closed above their respective averages. This “no cash” signal is unchanged from February, keeping the entire portfolio in an “invest” position for this longer time frame. However, momentum is slowing for a majority of the holdings. Three of the five funds are currently highlighted in yellow, indicating they finished the month within 2% of their moving average. While they remain in “invest” status for now, these narrow margins suggest that the portfolio is at a high risk of a trend reversal in the near future.

The S&P 500 and Moving Averages

The S&P 500 closed out March with a monthly loss of 5.1%, its largest monthly decline in a year and its third in the past four months. But let’s examine the index through the lens of moving averages.

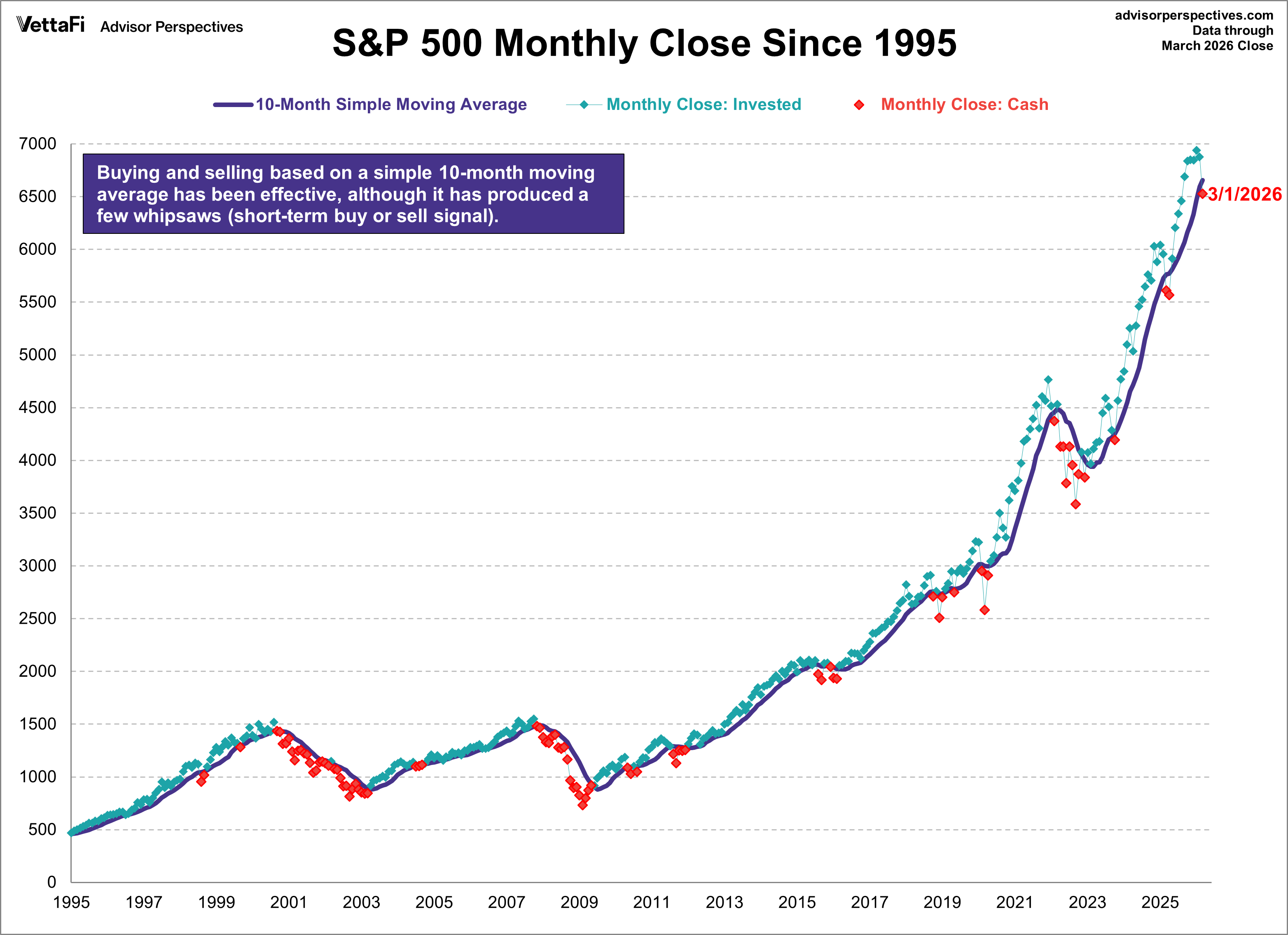

Buying and selling based on a moving average of monthly closes can be an effective strategy for managing the risk of severe loss from major bear markets. In essence, when the monthly close of the index is above the moving average value, you hold the index. When the index closes below, you move to cash. The disadvantage is that it never gets you out at the top or back in at the bottom. Also, it can produce the occasional whipsaw (short-term buy or sell signal), which was seen most recently in 2020.

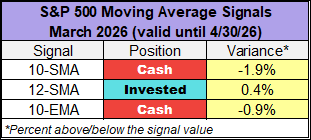

Nevertheless, a 10- or 12-month simple moving average (SMA) strategy would have ensured participation in most of the upside price movement since 1995 while dramatically reducing losses. For confirmation, here is a chart of the S&P 500 monthly closes since 1995 with a 10-month SMA. In March, the S&P 500 took a sharp downturn, closing 1.9% below its 10-month SMA, resulting in the index’s first “cash” signal in eleven months.

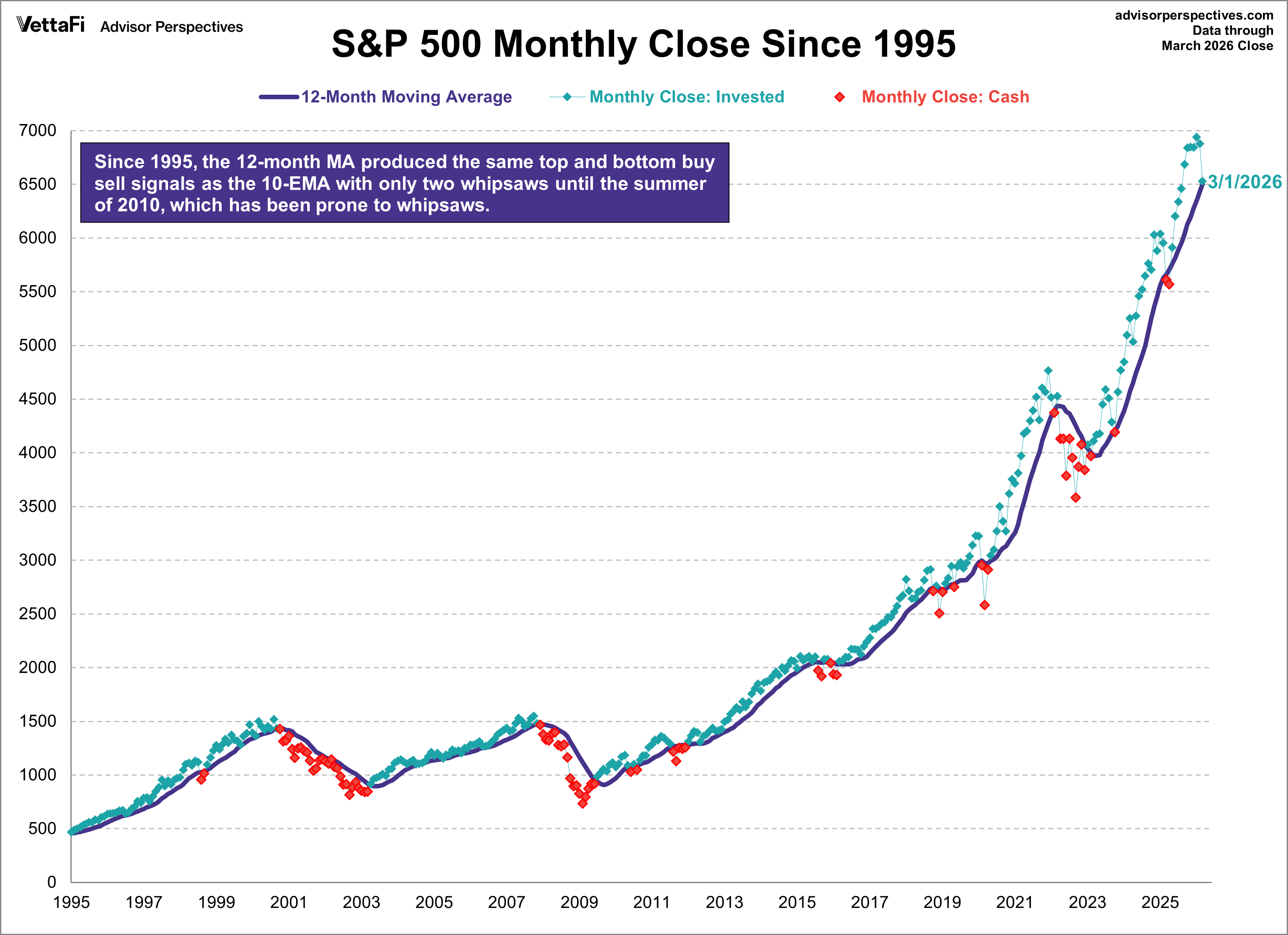

To further demonstrate, the next chart uses the 12-month variant. By using 12-months instead of 10, the moving average becomes slightly less volatile. Still, we can see that this is just as, if not more, effective in reducing losses. In March, the S&P 500 closed 0.4% above its 12-month SMA, marking its eleventh consecutive “invest” but its smallest variance (spread) over that same time frame.

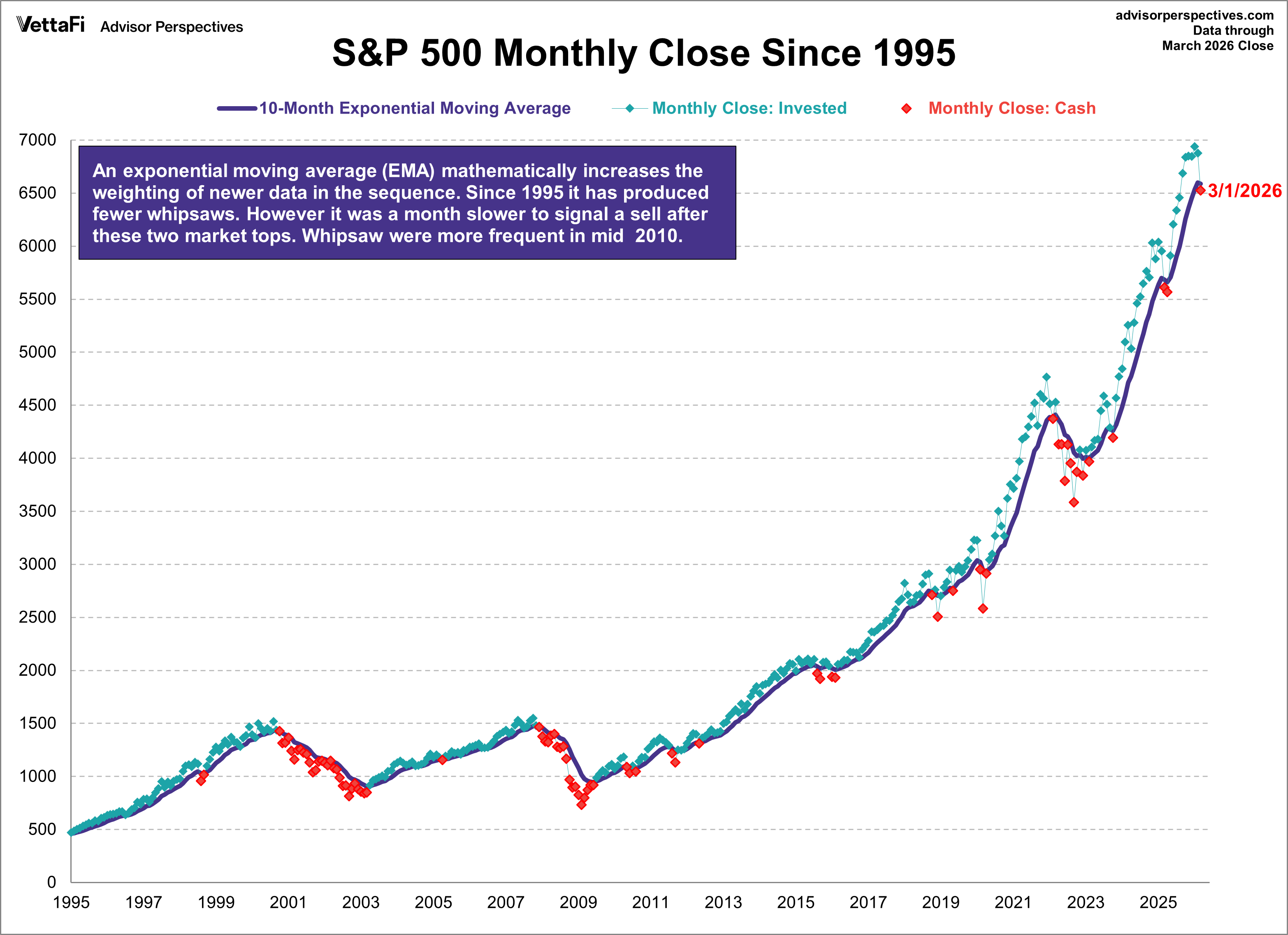

The next chart uses one more variation to the moving average strategy. The chart shows the 10-month exponential moving average (EMA), which is a slight variant to the simple approach used in the previous two charts. This version mathematically increases the weighting of newer data in the 10-month sequence. Since 1995 it has produced fewer whipsaws than the equivalent simple moving average. However, it was one month slower to signal a “sell” after the two market tops in 2000 and 2007. In March, the S&P 500 closed 0.9% below it’s 10-month EMA, marking its first “cash” position in eleven months.

To summarize, two of the three approaches closed below their respective moving averages and therefore reversed to a “cash” position at the end of March.

Moving Averages Effectiveness

A look back at the 10- and 12-month moving averages in the Dow during the Crash of 1929 and Great Depression shows the effectiveness of these strategies during those dangerous times.

The Psychology of Momentum Signals

Timing works because of a basic human trait. People imitate successful behavior. When they hear of others making money in the market, they buy in. Eventually, the trend reverses. It may be merely the normal expansions and contractions of the business cycle. Sometimes the cause is more dramatic: an asset bubble, a major war, a pandemic, or an unexpected financial shock. When the trend reverses, successful investors sell early. The imitation of success gradually turns the previous buying momentum into selling momentum.

Implementing the Moving Averages Strategy

Our illustrations from the S&P 500 are just that — illustrations. We use the S&P 500 because of the extensive historical data that’s readily available and the index signals give a general sense of how U.S. equities are behaving. However, followers of a moving average strategy should make buy/sell decisions on the signals for each specific investment, not a broad index. Even if you’re investing in a fund that tracks the S&P 500 (e.g., Vanguard’s VFINX or the SPY ETF) the moving average signals for the funds will occasionally differ from the underlying index because of dividend reinvestment. The S&P 500 numbers in our illustrations exclude dividends.

The strategy is most effective in a tax-advantaged account with a low-cost brokerage service. You want the gains for yourself, not your broker or your Uncle Sam.

Valid until the market close on April 30, 2026.

For more news, information, and analysis, visit VettaFi | ETF Trends.

Originally published on Advisor Perspectives.

As a regular feature of this website, we update the signals at the end of each month.

Note: For anyone who would like to see the 10- and 12-month simple moving averages in the S&P 500 and the equity-versus-cash positions since 1950, click here for an Excel file (xlsx format) of the data. Our source for the monthly closes (Column B) is Yahoo! Finance. Columns D and F show the positions signaled by the month-end close for the two SMA strategies.

Footnote on calculating monthly moving averages: If you’re making your own calculations of moving averages for dividend-paying stocks or ETFs, you will occasionally get different results if you don’t adjust for dividends. For example, in 2012 VNQ remained invested at the end of November based on adjusted monthly closes, but there was a sell signal if you ignored dividend adjustments. Because the data for earlier months will change when dividends are paid, you must update the data for all the months in the calculation if a dividend was paid since the previous monthly close. This will be the case for any dividend-paying stocks or funds.